Core Inflation Data Raises Questions Over TCMB Rate Path

faiz-yukselen

faiz-yukselen

Türkiye’s latest inflation data showed persistent price pressures despite signs of moderation in some core indicators. Seasonally adjusted consumer prices posted their strongest monthly increase since January 2025, driven largely by food and energy costs. Analysts from BBVA and ING say the data complicates the outlook for the Central Bank of the Republic of Türkiye (TCMB), with markets closely watching whether policymakers will begin easing later this year.

Strong increase in seasonally adjusted inflation

Türkiye’s seasonally adjusted Consumer Price Index (CPI) rose 2.76% month-on-month in February, marking the strongest monthly increase since January 2025.

According to special CPI indicators released by the Turkish Statistical Institute (TÜİK), the overall seasonally adjusted inflation rate also registered a 2.76% monthly rise.

A breakdown of core indicators showed mixed signals:

-

Index B (excluding unprocessed food, energy, alcoholic beverages, tobacco and gold) increased 2.40%

-

Index C (excluding energy, food and non-alcoholic beverages, alcohol, tobacco and gold) rose 1.80%

Across major spending categories, price increases were led by food and services:

-

Food and non-alcoholic beverages: +5.34%

-

Energy: +1.97%

-

Core goods excluding energy and food: +0.88%

-

Services: +2.69%

The data highlights the continued role of food inflation as a key driver of overall price pressures in the Turkish economy.

Doomsday Clock: Energy Shock and the Economic Stakes for Türkiye

BBVA: Headline inflation remains under pressure

In its latest assessment, BBVA Research said headline inflation in Türkiye remains under upward pressure, largely due to elevated food prices.

The bank noted that Ramadan-related demand may have also contributed to recent price increases. However, relatively moderate price movements in core goods suggest that the broader deterioration in inflation dynamics remains somewhat contained.

According to BBVA’s analysis:

-

Seasonally adjusted monthly inflation eased slightly from 2.84% to 2.75%

-

Despite the marginal improvement, price pressures remain strong overall

Core inflation moderating but services remain sticky

BBVA analysts noted that core inflation indicators show some signs of slowing, particularly in goods prices.

After accelerating in January due to widespread price adjustments at the start of the year, core goods inflation fell to around 0.5% in February.

However, services inflation remains elevated, reflecting ongoing cost pressures and structural rigidity in service-sector pricing.

The report estimates that services inflation remained around 2.7% monthly, highlighting the difficulty of bringing inflation down quickly.

Key indicators monitored by the TCMB signal risks

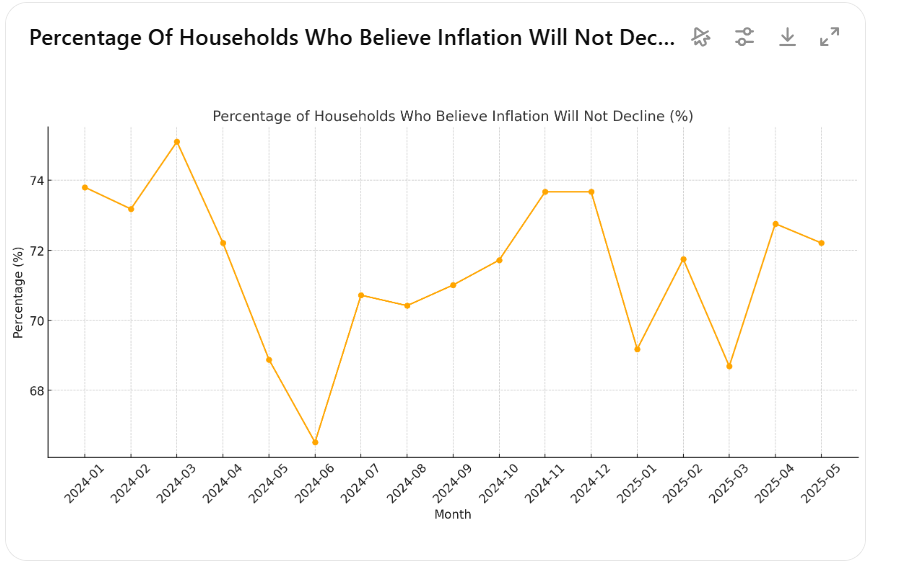

Several indicators closely monitored by the Central Bank of the Republic of Türkiye (TCMB) continue to suggest persistent inflationary pressures.

One of the most important metrics is median inflation, which rose to 2.2%, approaching levels seen early last year.

According to BBVA, several factors continue to pose risks to the disinflation process:

-

Domestic demand has not fully cooled

-

Inflation expectations remain elevated

-

Service-sector pricing remains sticky

Energy prices pose additional upside risks

Geopolitical tensions in the Middle East and rising energy costs are also creating new inflation risks.

According to BBVA estimates, a 10% increase in energy prices could add roughly 1–1.5 percentage points to headline inflation over a one-year period.

Energy costs therefore remain one of the most significant variables affecting Türkiye’s inflation outlook in the coming months.

ING: TCMB likely to hold rates in March

Following the February inflation release, economists at ING said they expect the TCMB to keep its policy rate unchanged at 37% at its March meeting.

The bank believes policymakers may begin a cautious easing cycle later in the year if inflation trends evolve as expected.

Under ING’s baseline scenario:

-

The central bank could start gradual rate cuts later in 2025

-

The policy rate may fall to around 30% by the end of the year

However, analysts stress that risks to the rate path remain skewed to the upside, meaning policy easing could be delayed if inflation surprises continue.

ING raises year-end inflation forecast

ING also revised its year-end inflation forecast for Türkiye upward to 25% following the February data release.

The bank cited several factors behind the revision:

-

Persistent pressure from food prices

-

Rising energy costs

-

Continued uncertainty in global oil markets

These dynamics are expected to complicate price stabilization efforts and could slow the pace of disinflation.

Markets watching TCMB policy signals

The latest data suggests that while Türkiye’s disinflation process continues, it remains fragile.

For the TCMB, policymakers face a delicate balancing act between:

-

Anchoring inflation expectations

-

Maintaining tight financial conditions

-

Avoiding excessive pressure on economic activity

As a result, the March Monetary Policy Committee meeting will be closely watched for signals about the timing and pace of future interest-rate cuts.

Author: PA Turkey Editorial Desk, CNBC-Turkey, Investing, ParaAnaliz