Equity Strategy: The state of Turkish markets amidst policy normalization

borsa

borsa

An Overview – Macro Outlook

Risk perception continues to improve as economic policies normalize

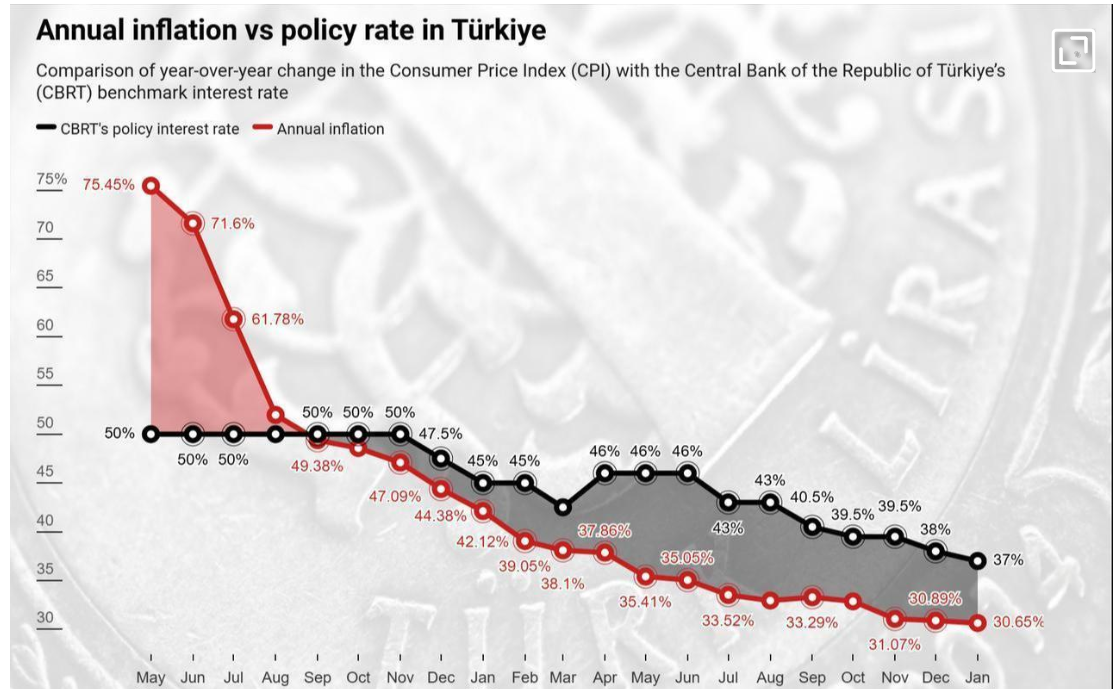

- The CBRT, as expected, initiated the rate hike cycle at its MPC meeting on June 22nd, highlighting inflationary risks. However, the 650 and 250 basis point interest rate hikes in June and July did not meet market expectations. After the modest policy rate hike at the MPC meeting on June 22nd, the USD/TL exchange rate immediately rose to 26.00 levels from around 23.50 before reaching levels in the 27.00s in the following days. As a result, the rise in the USD/TL rate after the election period amounted to roughly 40%. While gradual depreciation in the TL was within our macro scenario (as we shared in our strategy report published on June 20th), the pace of depreciation exceeded our expectations, which can be attributed to the rate hikes falling well below market expectations.

- Following the CBRT’s 750 bps hike, with the 1.8 coefficient based on the reference rate (currently 31.3%), the upper boundary for commercial loan rates has risen from roughly 38% to 56%. Accordingly, in the coming days, we might observe rapid increases in both loan rates and TL deposit rates (over 40% for deposits and over 50% for loans).

- Despite now elevating the policy rate to the presumed upper boundary of 25%, the CBRT continues to stress that monetary tightening will be further strengthened as much as needed, which implies the potential for ongoing rate hikes. In that manner, we believe that the policy rate could be raised to around 35% over the next few months.

- The government implemented a series of tax hikes to control the rapidly deteriorating budget deficit. Although we had already expected various tax hikes, particularly the 200% excise tax rate increase on gasoline, significantly exceeded our assumptions.

- Considering the spike in the currency and the magnitude of tax hikes exceeding our expectations, the indirect effects of the massive fuel price hikes (now reached about 100%), and the deterioration in pricing behaviour caused by all these developments, we had revised our year-end CPI inflation forecast from 55% to 69% on July 26. Nevertheless, the current outlook suggests that CPI inflation could head towards the 70-80% range in the upcoming period. To achieve a sustained decline from that point onward, it will be critical to rein in domestic demand and prevent foreign exchange demand.

- To the extent that the TL deposit rates approach inflation expectations (which now surpasses 60%), downward pressure on the Turkish lira may alleviate in the upcoming period. Strengthening seen in international reserves since June and expected capital inflows from the Middle East can also limit the depreciation pressure on the TL. Yet, foreign trade dynamics and the inflation outlook are expected to continue exerting pressure on the exchange rate. Cumulative inflation has reached nearly 20% in the past two months, and in the coming months, monthly inflation rates of around 4-5% look probable, despite continued monetary tightening. This could contribute to the “exchange rate – inflation – wage increase” spiral. At a time the CBRT encourages exits from the FX-protected deposit scheme (KKM) and reversals from KKM will be intensive, potential foreign exchange demand by individuals can also be an additional pressure factor on the exchange rate.

- Taking all the factors mentioned above into account, we anticipate (assume) the USD/TL rate at 29.50 by the end of the year, with risks to the upside.

- Despite the weakness in exports and industrial production, we see that the growth outlook is driven by the service sectors with the robustness in domestic demand. While we expect the upward trend in loan rates to limit domestic demand, the current inflationary environment may continue to support the tendency to pull forward demand. However, a significant factor supporting this trend was that credit card and cash advance overdue interest rates remained significantly below inflation (e.g.: overdue rate for cash withdrawals were 22% just a few months ago) , which supported financing of daily expenses. With the recent increases in the policy rate, the same rate increased to 59% and may rise towards 80%. In summary, we believe that this upward trend may lead to a sharp slowdown in domestic demand, especially from the last quarter onwards, which may curtail GDP growth to a range of 1-2% in 4Q23. Despite this potential pullback, we project 2023 GDP growth at around 3.5%, aided by the growth performance in the first half of the year.

- 12-month rolling C/A deficit may start declining after July due to reductions in gold and energy imports. As such, we expect the 12-month rolling C/A deficit to decline from the current USD56.5bn to some USD50bn by end-2023, and potentially to USD40-45bn levels by 1Q24.

- We believe that a possible improvement in credit ratings may be postponed to 2024, especially for Fitch and S&P. Yet, we also believe that there could be improvements in the outlook from all three agencies in 2023.

An Overview – Equity Outlook

Time to be more selective.

- We have been positive on Turkish equities since mid-May 2023. The key reasons for our view has been: (1) a weak market ahead of the elections, (2) the end of election uncertainty, and (3) a newly appointed macro team hinting relatively more orthodox economic policies.

- Since then the BIST-100 index rose by 67% (29% in USD terms) helped by (1) excessively discounted equity valuations, (2) the lack of alternative investment vehicles with the most popular deposit product offering negative real rates, (2) in general, firms continuing to post solid results and cash generation thanks to front loaded consumer demand in order to avoid higher priced future purchases and the normalization in the FX that supported the profitability’s of exporters. CDS spreads fell from mid 500s to mid 300s in due course.

- We believe, going forward, at current valuations, the impact of the amount of catalysts may be lessening. Turkish stocks still remain attractively valued, and likely strong earnings momentum creates further potential for upgrades once third quarter results are released. Yet, the magnitude of the upgrades could be less than the past 12 quarters. Moreover, while current deposit rates still hover around the mid 30s, well below the 12 month forward looking CPI rates, if the CBTR continues to raise rates determinately, it would create a major challenge for equities. Hence, we believe, the return/risk ratio is materially lower than a few months ago. We believe, a further decline in overall risk premium and higher international flow are key for Turkish equities to continue their sustainable performance.

- In terms of our estimates and comparable multiples (adjusted for CPI) the following is what we observe: Peer country 2 year average earnings growth expectations appears to be recovering from negative territory, while most of Turkiye’s negative trajectory is expanding. In the meantime, in terns of multiples, Turkiye’s EV/EBITDA discount has contracted from 57% 3 months ago, to 40%.

Raising BIST-100 target to 9,975 – upside 24%.

- Consequently, our upside is 33% for Banks and 23% for industrials. We use a RFR of 25% in our DCF models and cut them gradually each year based on our macro assumptions, which could create a downside risk on fair value estimates in case of a prolonged higher interest rate environment. On the other hand, a number of firms that we recommend in our model portfolio continue to provide substantial additional upsides.

Our Model Portfolio: Garanti and MLP Care, taking profit in Akbank and Yapı Kredi.

- We are adding Garanti based on the fact that leading indicators point to a superior quarter compared to the peers.

- MLP Care is added based on the recent health practice pricing revision (52% increase in healthcare services) along with expected synergies from the new hospital in Hungary. We believe our estimates and fair value estimate of the Company to be conservative.

Gedik Investment Research

Phone: +90 212 385 4200

www.gedikyatirim.com.tr

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: https://www.facebook.com/realturkeychannel