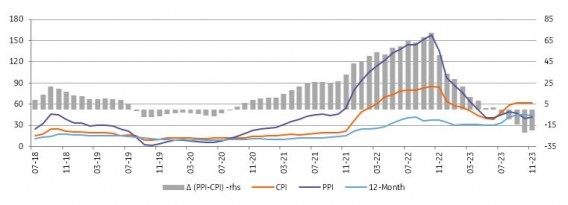

With another better-than-expected monthly reading at 3.3% (vs the consensus at 3.9% and our call at 3.8%), annual inflation in Turkey recorded a slight increase to 62% from 61.4% a month ago. The data reflect elevated upward pressures in services and the impact of natural gas prices. October PPI, on the other hand, stood at 2.8% MoM, translating into 42.2% YoY. The decline in annual PPI from close to triple digits at the end of last year shows improvement in cost pressures despite a Year-on-Year increase in the Turkish Lira equivalent of import prices lately due to commodity price developments and exchange rate increases.

Core inflation (CPI-C) came in at 1.96% MoM, inching up to 69.9% on an annual basis on the back of pricing behaviour, exchange rate developments, adjustments in administered prices and inertia in services. However, the underlying trend (as measured by 3m-ma, annualised percentage change, based on seasonally adjusted series), which dropped in October, maintained its recovery in November with a continued decline in not only the core but also the headline rate of goods and services inflation.

Inflation outlook (%)

Source: TurkStat, ING

In the breakdown, all main expenditure groups, with the exception of clothing, positively affected the headline:

· Among them, housing turned out to be the major contributor with 1.44ppt due to natural prices as households exceeded the free natural gas usage limit. Accordingly, energy inflation jumped to 21.2% from 11.6% a month ago.

· This was followed by food with 0.74ppt, though annual group inflation moderated to 67.2% (vs the CBT assumption at 66.7% in the latest inflation report release) on the back of both processed and unprocessed food. However, price pressures in processed food were still high, with the second-largest November increase in the current inflation series.

· 33ppt contribution, on the other hand, was attributable to alcoholic beverages and tobacco with adjustments in cigarette prices. On the flip side, clothing recorded a slight price decline on the back of seasonality.

As a result, goods inflation moved slightly up to 52.1% YoY, while core goods inflation receded to 52.2% YoY. Annual inflation in services, which is significantly influenced by domestic demand and wage hikes, maintained its uptrend and reached another peak at 89.7% YoY, attributable to the continuing rise in rents, transportation and telecommunication services.

Overall, annual inflation has remained in the 61-62% range for the last three months as pass-through from the post-election adjustment in FX, wages and taxes is reflected in the prices. The monthly trend of inflation may continue to improve if:

· currency stability is maintained,

· adjustments in wages and administered prices prioritize inflation concerns,

· the impact of geopolitical issues on oil prices remains under control

· domestic demand sustains its moderation path.

We expect inflation to remain elevated until mid-2024, with further increases above 70% on seasonal effects in January and unfavourable base effects in May. The second half of next year will likely see a sharp downtrend – reflecting this year’s high base and further impact of tighter policy, pulling inflation to 40-45% by the end of the year.

At the November MPC meeting, the CBT raised the one-week repo rate to 40.0%, providing guidance that:

· the pace of monetary tightening would slow

· the tightening steps would be completed in a short period of time,

· the monetary tightening required for sustained price stability would be maintained as long as necessary.

Accordingly, we expect that the interest rate hike process will be completed at 45.0% with more limited increases of 250 basis points in December and January meetings. However, better-than-expected inflation readings and currency stability may also lead the bank to end the hiking cycle after a single 250bp hike.

ING