Turkish GDP growth in 3Q turned out to be 5.9% year-on-year, better than market consensus, on the back of still strong private consumption despite a moderation compared with previous quarters, robust investment and accelerating government consumption. Net exports turned out to be a drag again. 3Q GDP translates into quarter-on-quarter growth at 0.3% after seasonal adjustments, showing momentum loss in comparison to a relatively 2Q strong reading at 3.3%.

The easing sequential performance is attributable to household consumption turning negative for the first time since the last quarter of 2020 and a negative contribution from stocks despite solid investment appetite and the supportive impact of net exports. Recent indicators on the other hand show that the gap between aggregate demand and supply that has led to significant pricing pressures is continuing to narrow, with gradual policy tightening since the elections. This should also be supportive for the external imbalances, with expected pressure on import demand.

We expect GDP growth this year to be 4.2% as momentum is still strong. We envisage a further slowdown to 2.5% for 2024, reflecting the full impact of the rate hikes. That said, the risks are to the upside – with the government’s latest Medium Term Plan (MTP) forecast at 4.0%, in addition to a continuing supportive fiscal stance and a potential recovery in foreign capital inflows.

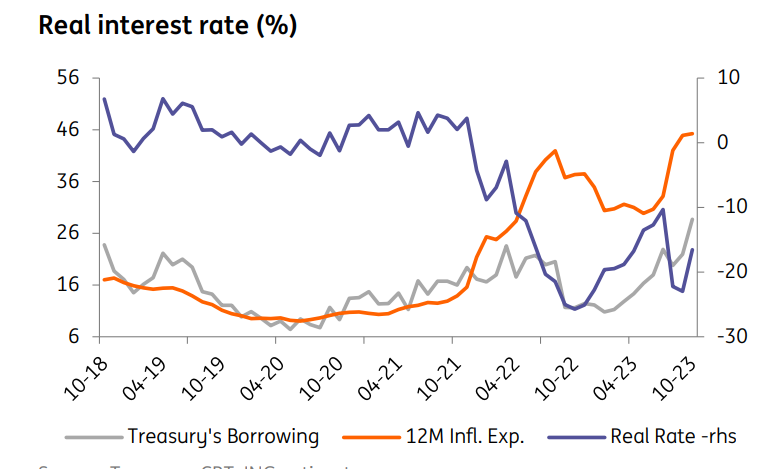

While the CBT indicates that pass-through from the post-election adjustment in FX, wages and taxes has been ‘largely completed’, deterioration in pricing behaviour, exchange rate related risks, and the possibility of adjustment in administered prices hint that CPI inflation will likely remain elevated in the near term. On a positive note, the underlying trend for core and headline CPI has started to improve. The continuation of recent stability in the Lira, moderation in domestic demand and consumer subsidies for electricity and natural gas prices will also be supportive for the outlook.

Regarding PPI, the decline in the annual figure from close to triple digits at the end of last year highlights a recovery in cost pressures despite an increase in the TL equivalent of import prices. For CPI, we expect annual inflation to continue to rise for the remainder of this year, to above 65% – households are expected to exceed the free natural gas usage limit, which in turn will boost monthly inflation.

Inflation will likely remain elevated until mid-2024, with further increases above 70% on seasonal effects in January and unfavourable base effects in May. The second half the year, on the other hand, will likely see a sharp downtrend – reflecting this year’s high base and further impact of tighter policy, pulling inflation to 42% at year-end.

From ING CEEMEA report ” Directional Economics: CEEMEA in 2024” , author: Murat Mercan, Chief Economist

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/