BoFA on Turkish banks: The Great Normalization – Buy private banks

bankalar

bankalar

Risk-reward is appealing

‘Normalization’ is probably the best word to describe the ongoing dynamics in the Turkish banking system. Regulations that have played a key role in growth dynamics, asset allocations and key interest rates over the past two years have been partially simplified. We think recovery in core spreads and an improved fee base will continue to support revenues while we see asset quality risks as manageable. With +30% sustainable RoEs we believe Turkish private banks offer good value. We are buyers of Isbank, Akbank, Garanti and Yapi, and have Underperform ratings for state peers, Halk and Vakif.

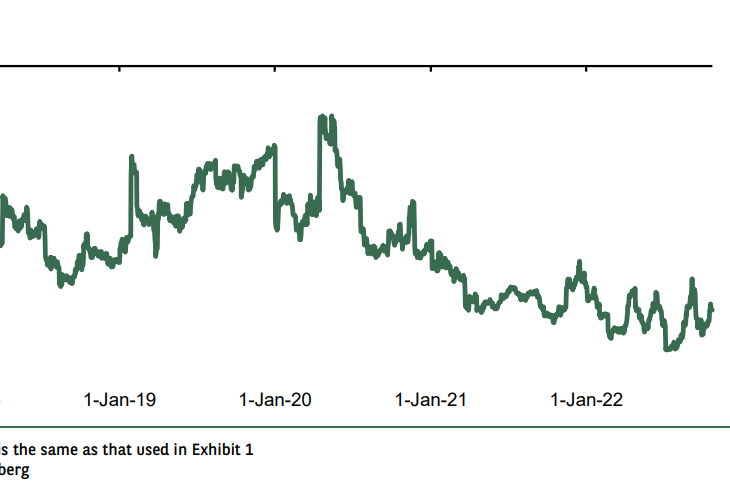

Negative real loan growth in 2024E…

We see TRY loan growth averaging slightly above 30% in 2024 (broadly in line with what annualized monthly growth caps suggest) and expect real loan growth to resume in 2025. Despite the high nominal growth rates in recent years, credit penetration and loan to deposit ratios have declined to levels not seen for more than a decade. This does not indicate a secular growth story, under current macro circumstances, but it might indicate a good starting point for the post-tightening period.

…but core revenue margins to remain intact

We believe TRY funding costs will remain elevated driven either by regulations or market dynamics. Regardless, the core spread recovery is likely to be sustained (vs. the current low base) given the level of lending rates. Despite diminishing CPI linkers contribution, normalizing trading gains and absence of various sources of activity-related fee income, we expect core revenue margins to remain resilient in 24E and expand further in 25E.

Asset quality is more resilient than you think

We agree that the current low NPL and CoR levels are unsustainable, and a new cycle is around the corner. However, we are less concerned vs. previous cycles. Turkish private banks have deliberately given away market share, increased coverage, and accumulated capital since 2018. Our stress test shows that they are well-equipped to stomach extreme scenarios without the need for capital or even reporting P&L losses.

Additionally, there are several mitigating factors: 1) FX mismatch is no longer a key risk for corporates; 2) household balance sheets have strengthened given gains from FX deposits & equities vs. negative real rates on loans; and 3) the average ticket size of unsecured loans is small and a large portion is distributed to salary clients.

Positive on private banks – Buy ratings across the board

We believe Turkish private banks’ RoEs should settle north of 30%. This is higher than our long-term CoE assumptions. With c65% total return in TRY terms or +25% in USD terms, we think valuations are attractive. We have Buy ratings on Akbank (upgraded from Neutral), Isbank (upgraded from Underperform), Garanti and Yapi. We reiterate our Underperform ratings on Halk and Vakif given lower profitability, limited capital buffers and above-sector PB multiples.

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/