MORNING NOTE: Markets Caught Between War and Peace

piyasa satis

piyasa satis

Global markets remain stuck in a fragile “neither war nor peace” environment as tensions in the Middle East persist. Disruptions in the Strait of Hormuz continue to push oil prices higher, weighing on risk appetite and leaving investors cautious ahead of key central bank decisions.

A Fragile Ceasefire, Rising Tensions

The uneasy ceasefire in the Middle East is holding—for now—but underlying tensions continue to escalate. Iran’s tightening control over the Strait of Hormuz has effectively constrained one of the world’s most critical energy corridors.

- Roughly 20% of global oil and LNG supply flows through Hormuz

- Iran’s actions are seen as retaliation against U.S. naval restrictions

- U.S. intervention in tanker movements has intensified the standoff

Markets are struggling to find direction in this ambiguous environment—where escalation risks remain high, yet a full-scale conflict has not materialized.

Global Trade Rethinks Its Dependencies

Recent developments have exposed the vulnerability of global trade to chokepoints like Hormuz. As a result, attention is increasingly turning to alternative routes.

The “Middle Corridor” (linking China to Europe via Central Asia and Türkiye) is gaining traction as a strategic logistics route.

Türkiye is emerging as a key transit hub, benefiting from:

- Strategic geography

- Expanding infrastructure

- Growing role in East-West trade flows

While Hormuz remains irreplaceable for energy transport in the short term, diversification efforts are expected to accelerate once tensions ease.

Europe’s Strategic Ambiguity on Türkiye

European Commission President Ursula von der Leyen recently grouped Türkiye alongside China and Russia in strategic discussions—raising eyebrows.

Former European Council President Charles Michel pushed back, emphasizing:

- Türkiye’s critical NATO role

- Its importance in migration management

- Its position as an energy corridor

These contrasting views highlight growing fragmentation within Europe’s foreign policy stance.

ANALYSIS: When Will the CBRT Cut Rates? Global Energy Shock Clouds Outlook

Markets React: Oil Up, Risk Appetite Down

Geopolitical risks continue to ripple through global markets:

- Brent crude climbed toward $105–106 per barrel

- Tech-heavy Nasdaq index declined करीब 1%

- Overall risk appetite weakened

However, not all sectors are under pressure. Intel stood out with a strong earnings outlook driven by demand for AI-focused data center chips, sending its stock up nearly 19% in after-hours trading.

Gold, Silver and Crypto Diverge

Recent price action across asset classes shows diverging trends:

- Gold fell from $4,900 to around $4,675

- Silver dropped nearly $10 in five sessions to $74

- The U.S. dollar strengthened modestly

- EUR/USD retreated to around 1.1670

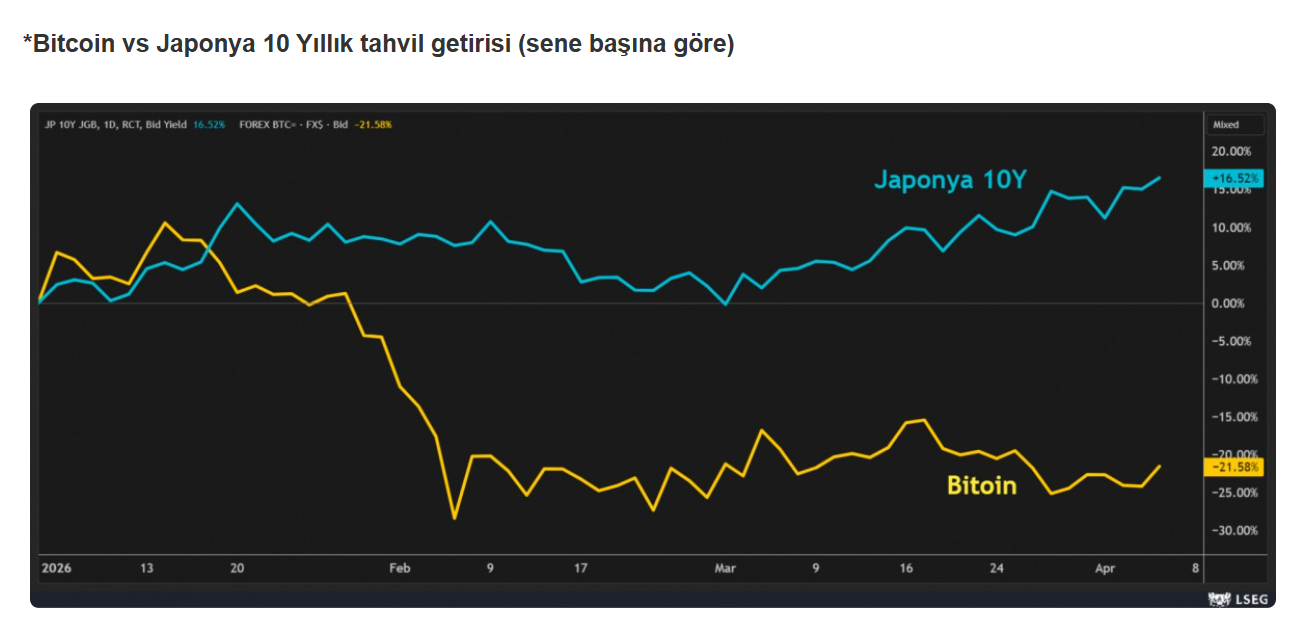

Meanwhile, Bitcoin continues to outperform:

- Tested $80,000 recently

- Holding near $78,000 despite market uncertainty

The BTC-to-gold ratio is showing early signs of shifting in Bitcoin’s favor.

Silver Outlook: High Volatility, High Potential

A striking projection from Bank of America suggests silver could trade between $135 and $309 by end-2026.

Key drivers include:

- Persistent supply deficits (expected for a sixth consecutive year)

- Dual demand from investment and industry

- Structural constraints in mining supply

Silver’s hybrid nature makes it more volatile—but also potentially more explosive.

NATO Chief Rutte Praises Türkiye’s Defense Industry After Aselsan Visit

Central Bank Watch: Türkiye Holds Steady

Central Bank of the Republic of Türkiye kept rates unchanged at its April meeting:

- Policy rate: 37%

- Lending rate: 40%

- Borrowing rate: 35.5%

The decision signals a careful balancing act between:

- Slowing economic momentum

- Persistent inflation risks

Markets interpreted the stance as moderately supportive of growth.

Domestic Market Snapshot

- BIST 100 expected to remain under pressure

- USD/TRY approaching 45.00

- CDS spreads around 240 basis points

- 2-year bond yields near 40%

Short-term funding rates are likely to remain elevated, with gradual easing possible under a favorable scenario.

Asia Mixed, Global Mood Cautious

Asian markets showed mixed performance:

- Japan gained on tech strength

- South Korea declined around 1%

The broader picture remains one of uncertainty, driven by stalled U.S.-Iran negotiations and persistent geopolitical risks.

All Eyes on the Fed

The upcoming decision by Federal Reserve on April 29 is the next key catalyst.

Markets have largely abandoned expectations for near-term rate cuts, focusing instead on:

- Inflation persistence

- Energy-driven cost pressures

Upcoming data points include:

- UK retail sales

- Germany’s IFO business climate index

Conclusion: A Market in Limbo

Global markets are navigating a complex landscape:

- No full-scale war—but no lasting peace

- Elevated oil prices sustaining inflation risks

- Central banks maintaining cautious stances

Investors are likely to remain in “wait-and-see” mode, closely watching geopolitical developments and policy signals.

By Emre Degirmencioglu, Kıbrıs İktisat Bankası

Related articles

‘Oil tanker traffic jam’ increases in Istanbul amid EU sanctions

Erdoğan Likens Netanyahu to Hitler, Accuses Israel of Fueling Regional Instability

OECD Lifts Türkiye Growth Forecast but Warns Inflation Risks Remain