ANALYSIS: Current Account Deficit Widens and Reserves Dip, but Financing Remains Abundant

Account Deficit of Turkey

Account Deficit of Turkey

By Atilla Yesilada

The Turkish economy is currently navigating a complex dual reality. While geopolitical tensions in the Middle East drive up energy costs and pressure central bank reserves, the country is simultaneously experiencing one of its most robust periods of external financing in years. This influx of liquidity provides a critical cushion for policymakers defending the Turkish Lira.

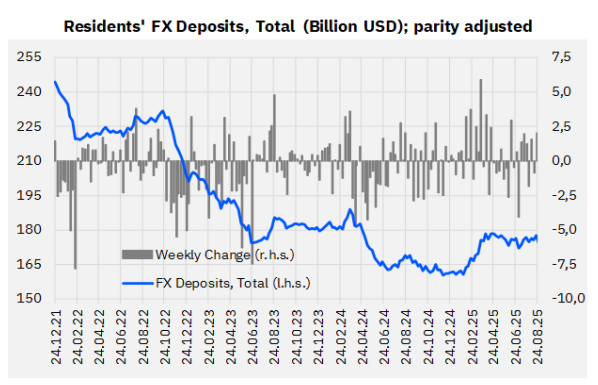

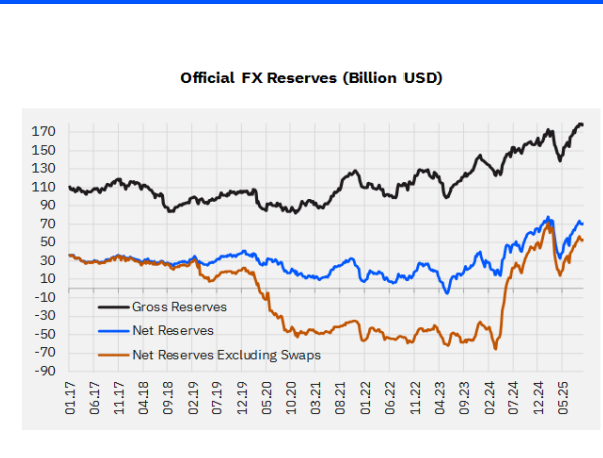

Reserve Volatility: CBRT Interventions vs. Gold Valuation

During the week of March 6, net reserves (excluding swaps) saw a decrease of $13.6 billion. When adjusting for the positive $2.5 billion impact of rising gold prices, the net drop in reserves stands at $11.5 billion. According to CBRT Analytical Balance sheet data as of March 11, we estimate a $6.5 billion decline in gross reserves and a $7.8 billion drop in reserves excluding swaps. Since the beginning of March, we calculate that the CBRT’s foreign exchange sales (excluding the gold effect) have reached $21.6 billion, totaling $26.5 billion since the start of the year.

Widening Deficits and Energy Price Risks

According to data from Akbank, following methodological revisions, the current account balance posted a deficit of $6.8 billion in January, exceeding market expectations. The 12-month cumulative deficit was revised to $30.1 billion for year-end 2025 (up from $25.2 billion) and reached $32.9 billion by January. Seasonally adjusted data points toward an annualized deficit trend of approximately $55 billion, or 3.0% of GDP.

Looking ahead, if Brent crude averages $90 in 2026, the additional external financing requirement driven by energy costs could reach $20 billion, potentially pushing the year-end current account deficit to $60 billion (3.3% of GDP).

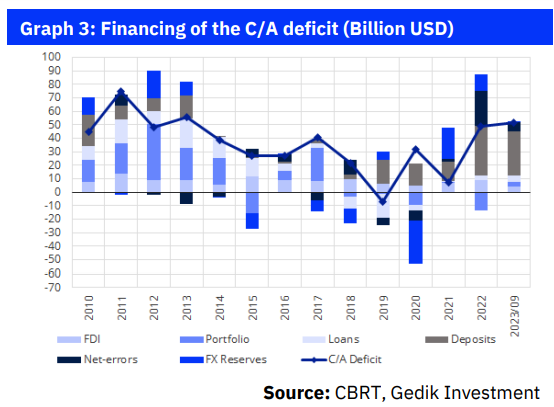

Record Capital Inflows: Portfolio and Other Investments

Despite the widening deficit, January saw a massive turnaround in capital flows. Portfolio investments recorded a net inflow of $8.4 billion—the highest since April 2013. This surge was primarily driven by an $8.5 billion appetite for debt securities.

Furthermore, the “Other Investments” category hit its highest level since May 2020 with $11.7 billion in inflows. Notable is the record $5.7 billion in deposits held by foreign banks within domestic correspondents. With long-term debt rollover rates at 167.2% for the banking sector and 214.4% for non-banking sectors, Turkey’s access to international liquidity remains exceptionally strong.

COMMENTARY

The expansion of the core current account deficit has reached concerning levels. The decision by Middle Eastern tourists to remain home and the looming increase in energy import bills suggest that the deficit will widen further in the coming months. According to Akbank, the deficit could exceed 4% of GDP this year—a level traditionally considered dangerous. However, there is no immediate reason to fear a currency crisis, as external financing remains highly abundant. As long as the conflict does not drag on into the peak summer months and cause a total collapse in tourism revenue, the CBRT can comfortably maintain its “Strong Lira” policy.

Additionally, the CBRT can always compensate for gross reserve losses by borrowing foreign currency deposits parked in banks via swaps. Consequently, the bank is unlikely to lose control over the exchange rate in the near term.

Naturally, “black swan” scenarios still exist. Reports of regional agents targeting international interests within Turkey could halt tourist flows entirely. Similarly, if Brent crude spikes to $150 per barrel and sustains that level, the CBRT would be forced into aggressive interest rate hikes to prevent a currency meltdown. In such a crisis, a strong Lira policy cannot be the only defense; immediate cuts in budget spending would be required to narrow the deficit. Turkey is entering a difficult period that will likely last until the summer. The government’s ability to resist pressure for mid-year wage hikes and energy price subsidies will be the deciding factor in preventing a flight from Lira deposits back into foreign currency.

Related articles

ANALYSIS: September current account in surplus, but what about the winter?

Weekly CBRT Data: Reserves, Deposits, and Capital Flows

Weekly Financial Developments – September 19: CBRT rebuilds FX reserves