Borsa Strategy: Can Borsa Istanbul Soar Higher?

borsa

borsa

Background: Post-Hormuz Scenarios Point to Gradual Commodity Normalization, but Risks Remain

Summary: A multi-scenario analysis of global commodity markets following the disruption in the Strait of Hormuz suggests a base case of gradual supply normalization. However, persistent geopolitical risks continue to cloud the outlook, with implications for inflation, interest rates, and global growth. For Türkiye, rising energy costs are expected to drive higher inflation and a wider current account deficit.

Four Scenarios Shape the Global Outlook

The analysis outlines four potential scenarios for global energy and commodity markets, driven primarily by geopolitical developments:

- Rapid normalization (15%)

- Gradual normalization (50%)

- Prolonged normalization (30%)

- Supply shock (5%)

The first two scenarios, accounting for 65% probability, تشير إلى a relatively constructive macro environment, while the remaining 35% represent downside risks with potentially asymmetric and more severe impacts.

Best-Case Scenario: Rapid Normalization

Under the “rapid normalization” scenario, a lasting ceasefire would allow supply chains to recover quickly.

This would likely lead to:

- A sharp decline in energy prices

- Easing inflationary pressures

- Stronger global growth

- Earlier interest rate cuts by central banks

In such an environment, risk appetite would improve, capital flows to emerging markets would accelerate, and the US dollar would weaken.

Global Diplomacy Winds Fuel Bullish Surge: BIST 100 Eyes New Records

Base Case: Gradual Adjustment

The most likely scenario, with a 50% probability, assumes a gradual normalization in commodity supply.

In this case:

- Global growth slows modestly but avoids recession

- Inflation remains elevated, though manageable

- Central banks maintain a “higher-for-longer” stance

As a result, global interest rates are expected to decline only slightly, the dollar is likely to remain relatively strong, and risk appetite will improve selectively.

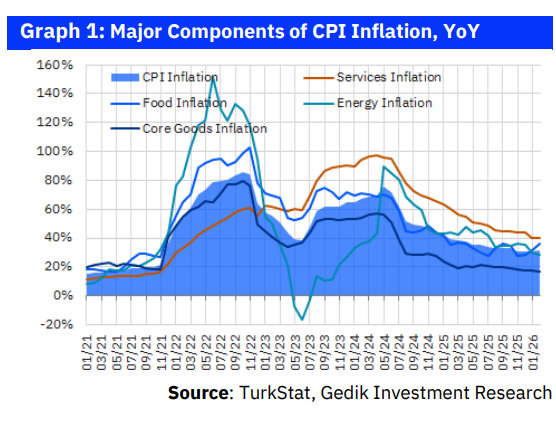

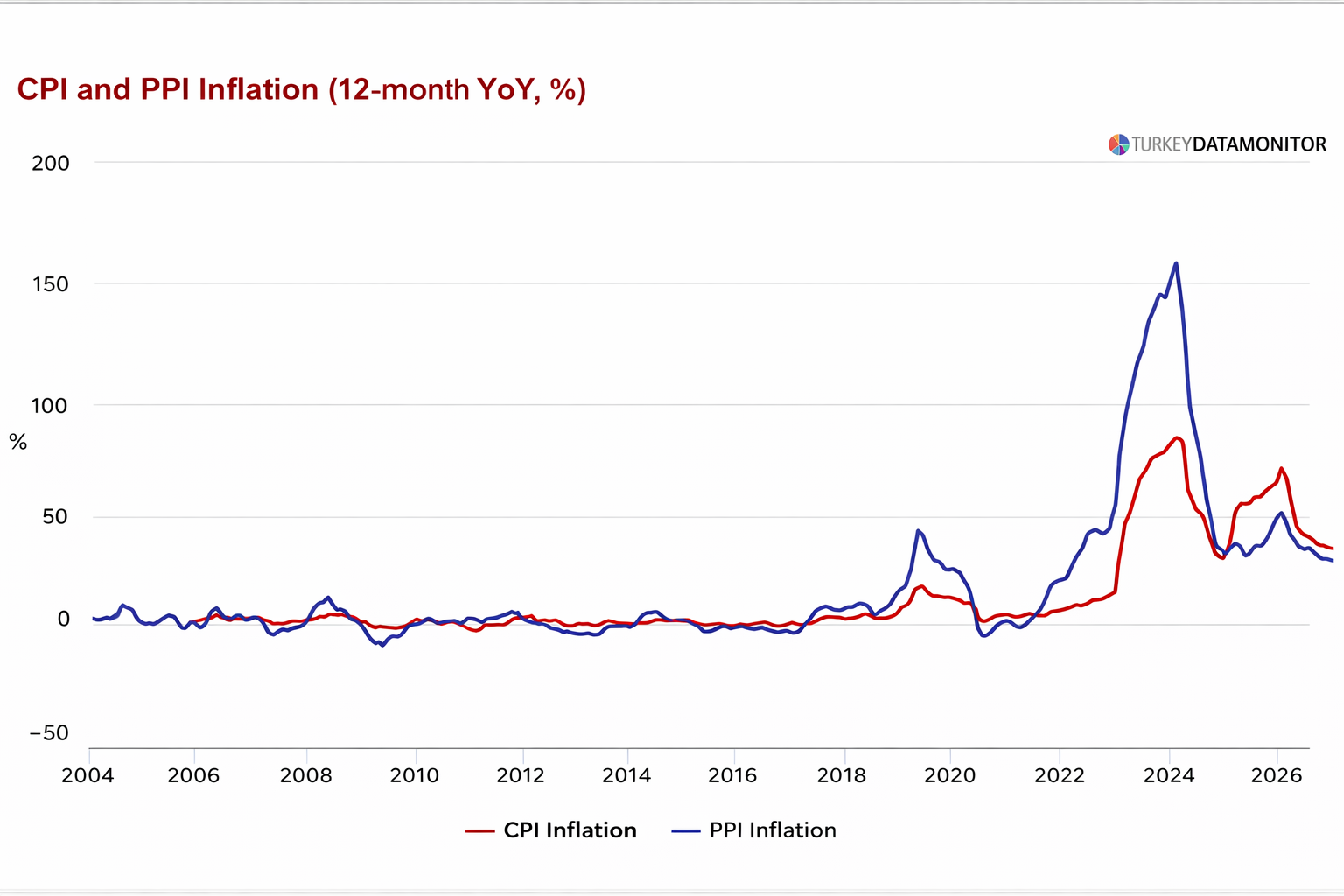

Türkiye Outlook: Higher Inflation, Delayed Easing

For Türkiye, the base scenario assumes Brent crude averaging around $80 per barrel through the remainder of the year.

Under these assumptions:

- Consumer inflation is expected to remain above 30% through late summer

- Year-end inflation is projected at around 29% (revised up from 25%)

- Interest rate cuts may be delayed to September or October

The policy rate is expected to end the year in the 34.5%–35% range. While rates are likely to remain unchanged in the near term, a potential hike of 150–300 basis points remains on the table depending on reserve dynamics.

Current Account Forecast Revised Higher

The analysis revises Türkiye’s 2026 current account deficit forecast upward from $35 billion to $55 billion, equivalent to around 3% of GDP.

Key drivers behind this revision include:

- Higher energy import costs

- An assumed 18%–20% increase in commodity prices

- Deterioration in services and primary income balances

Downside Scenarios: Stagflation Risks

Less likely but more impactful scenarios include prolonged normalization or a full supply shock driven by continued conflict.

In these cases:

- Energy prices remain elevated

- Global growth weakens significantly

- Inflation becomes more persistent

Central banks may be forced to delay rate cuts or even tighten policy again. In the worst-case scenario, global growth could slow sharply, accompanied by a broad risk-off move in financial markets.

Türkiye Assets Remain Geopolitically Sensitive

The outlook underscores Türkiye’s continued sensitivity to energy prices and geopolitical developments.

Under adverse scenarios:

- The current account deficit could widen further

- Inflation pressures would intensify

- Monetary policy may need to remain tighter for longer

Borsa Istanbul: Strong Performance, Uncertain Outlook

The BIST 100 Index has delivered a solid performance year-to-date:

- Up 19% in USD terms

- Up 24% in local currency

It has also outperformed the MSCI Emerging Markets Index on a relative basis.

Sector performance has been led by:

- Defense

- Oil and gas

- Utilities

while banking, real estate, and telecom sectors have lagged.

Earnings Outlook Revised Lower

Profit expectations for 2026 have been revised downward:

- Industrial EBITDA growth cut from 16% to 7%

- Net profit growth reduced from 29% to 13.8%

- Banking sector profit growth lowered from 30% to 8.3%

Upward revisions were concentrated in the oil and gas sector, while consumer, mining, automotive, and aviation sectors saw more significant downgrades.

Target Level: 17,580 for BIST 100

The report sets a target level of 17,580 for the BIST 100, implying a potential upside of around 24%.

Preferred sectors include:

- Oil and gas

- Food and food retail

- Apparel retail

Selective holding companies are also favored due to attractive valuations.

Conclusion: Balanced but Cautious Positioning

While the base case remains relatively constructive, the 35% probability assigned to adverse scenarios calls for a cautious investment approach.

The report recommends:

- Maintaining exposure to commodities and energy

- Limiting duration risk

- Taking a selective approach to equities

As geopolitical uncertainty persists, portfolio resilience and flexibility remain key.

By Gedik Invest

PA Turkey intends to inform Turkey watchers with diverse views and opinions. Articles in our website may not necessarily represent the view of our editorial board or count as endorsement.

Follow our English YouTube channel (REAL TURKEY):

https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/***

Related articles

Iran-Israel Tensions Fuel Economic Anxiety in Turkey

January Inflation Shock—Is the “Easy” Disinflation Over?

Turkish Lira to Reign Supreme: Economist Atilla Yeşilada Forecasts Strong TL Throughout 2026