Turkey’s Economy Signals Slowdown: Q2 Growth Concerns Mount

dusen-grafik

dusen-grafik

Early indicators for the second quarter suggest a significant deceleration in Turkey’s economic activity, with manufacturing and various service sectors showing signs of weakening.

Istanbul, Turkey – Preliminary data for Turkey’s economy in the second quarter of the year points to a marked slowdown in growth. The latest economic sentiment surveys for June, including the Economic Tendency Survey (ETS), Real Sector Confidence Index (RSCI), and Capacity Utilization Rate (CUR), all indicate a tangible loss of production and demand, particularly within the crucial manufacturing sector. This deceleration comes amidst ongoing global and domestic uncertainties that continue to negatively impact expectations, a trend further supported by the Central Bank of Turkey’s (CBRT) output gap estimates.

Confidence Indices Point Downward

Real Sector Confidence Index (RSCI): The RSCI, which reflects the general outlook of the manufacturing industry, declined in June after drops in April and May. It now sits below its historical average, underscoring a noticeable weakening in manufacturing during the second quarter. The monthly decrease was driven not only by the general outlook but also by reductions in total order indices over the last three months. Rising domestic and international market uncertainties continue to fuel concerns, leading to lower expectations for production volume and export orders.

Sectoral Confidence Indices (SCI): After increases in the first quarter, sectoral confidence indices showed a mixed picture in June following limited improvement in May, remaining below their first-quarter averages.

- The services sector confidence index saw a slight monthly improvement, yet future demand expectations continued to decline, suggesting the recovery in this sector isn’t yet firm.

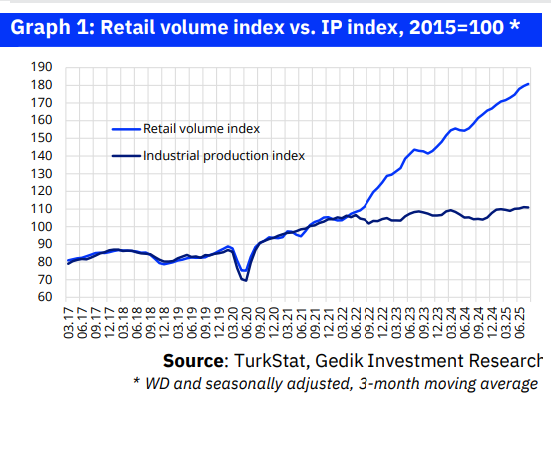

- The retail sector confidence index experienced a significant drop in June, hitting its lowest level since September 2024. This confirms signals of weakening domestic demand, particularly with a sharp fall in sales expectations for the next three months, highlighting challenges ahead for retail.

- The construction sector confidence index also decreased in June, indicating that May’s strong increase didn’t translate into a sustained recovery.

In summary, all confidence indices across the services, retail, and construction sectors remained below both their historical and first-quarter averages in Q2. This broadly signals an economy-wide slowdown, a view consistent with the CBRT’s recent Inflation Report, which projected below-potential growth for upcoming quarters.

Capacity Utilization Rate (CUR) Shows Declining Trend

The seasonally adjusted Capacity Utilization Rate (CUR) in the manufacturing sector, another key indicator of production weakness, fell by 0.7 percentage points to 74.4% in June. This figure is 1.9 points below its historical average, confirming the ongoing weakness in manufacturing’s main trend.

A closer look reveals that the CUR decline impacted small, medium, and large-scale firms alike. Notably, CUR for small-scale firms dropped to its lowest level since December 2020. While there was a limited increase in non-durable consumer goods, all other product groups saw declines. The CUR for intermediate goods, in particular, reached its lowest point since March 2023, suggesting the production slowdown is also impacting the input side.

At the sectoral level, the overall drop in manufacturing CUR was influenced by declines in major sectors such as automotive, machinery and equipment, and electrical equipment. Food and apparel sectors, which have a high share in industrial production and exports, also experienced decreased CURs.

However, there were some exceptions: the CUR in the basic metals industry increased monthly to its highest in four months. The other transport vehicles sector, which includes defense industry vehicles, saw its CUR continue to rise in June after a May increase, reaching an 11-month high and surpassing its historical average. This suggests this sector could significantly contribute to industrial production again. In contrast, the textile sector’s CUR showed a limited recovery in June after falling below 70% for the first time in nearly two years but remained weak.

Other Findings from the Economic Tendency Survey

Production Volume and Orders: The question regarding production volume over the last three months declined again in June after a flat May, remaining significantly below its long-term average. A notable decrease in investment goods was observed, with an overall quarterly production volume decrease in Q2.

Registered domestic market orders decreased in June, signaling a continued loss of momentum in domestic demand. Export orders, after a three-month decline, remained flat in June, showing a weak outlook below historical averages. Significant decreases were observed in both domestic and foreign market orders for investment goods.

Employment and Investment Tendency: Employment tendency decreased again in June after an increase in May. Investment tendency showed a limited increase after a four-month decline but couldn’t compensate for previous losses. These indicators suggest that firms are being cautious with their future employment and investment decisions.

Expectations: Manufacturing firms’ foreign order expectations have been declining for the past five months. While domestic market order expectations increased in June, both domestic and foreign order expectations have been below their long-term averages for the last four months. Cost and pricing expectations also continued to decline in June. The manufacturing industry’s 12-month producer price index (PPI) annual inflation expectation decreased monthly to 37.2%, but this expectation remains significantly above current PPI inflation. Potential increases in commodity prices could pose an upward risk to these expectations.

All these leading indicators clearly show that Turkey’s economy has entered a period of slowing growth in the second quarter, a trend that’s spreading across various sectors. Against these signals of deceleration, the steps taken to combat inflation and ensure macroeconomic stability will require careful consideration.

Related articles

Global Banks Forecast Rate Cuts by Turkey’s Central Bank in H2 2025

Turkish Industrial Output Flashes Mixed Signals: Annual Growth Holds Firm, But Quarterly Contraction Triggers Alarms

Timothy Ash: Turkey’s Economy Is on the Right Path, But Inflation Remains the Real Test