Fitch Turkey Director Kılınç: Rate Cuts Are Starting to Benefit Banks

bankalar

bankalar

Fitch Ratings’ Turkey Director Ahmet Kılınç said the Central Bank of Turkey’s (CBRT) recent rate-cut cycle has begun to produce positive effects for the country’s banking sector. In an interview with Bloomberg HT, he noted that the impact will become more visible between late 2025 and early 2026, as lower rates filter through to credit costs and profitability.

Early Signs of Recovery in Banking Margins

Kılınç said Turkish banks are showing strong performance in fee and commission income, while interest-rate cuts are beginning to support net interest margins and lending activity.

“We expect the positive impact of monetary easing to become clearer in the fourth quarter of 2025 and the first quarter of 2026,” he said.

Despite the improving trend, Fitch continues to monitor credit-quality risks, particularly in consumer loans and credit cards.

COMMENTARY: Brace for Impact: Why I’m Sounding the Alarm on the Turkish Economy and Global Bubbles

“NPL Ratio May Rise to 3%, But It’s Manageable”

According to Kılınç, the non-performing loan (NPL) ratio currently stands at 2.2%, with potential to rise toward 3%.

He said this increase would not indicate a systemic risk:

“The rise is mainly driven by retail credit and card loans, but these levels remain manageable.”

While the household NPL ratio is above historical averages, small-business (SME) loans remain below long-term norms. Fitch will continue to track SME loan performance and potential restructurings in the coming quarters.

Profitability Supported by Fees and Commissions

Kılınç noted that high risk costs remain the main factor limiting bank profitability but added that the outlook is improving.

“Risk costs will stay elevated in the short term, but sentiment should turn more optimistic by the second quarter of 2025,” he said.

Regulatory controls continue to shape both credit growth and net interest margins (NIMs). Still, strong fee and commission income is expected to remain a key profit driver. Fitch forecasts that Turkish banks’ earnings in 2025 will exceed 2024 levels, with a more pronounced rebound in 2026.

“Sustainable Growth and Disinflation Are Our Base Case”

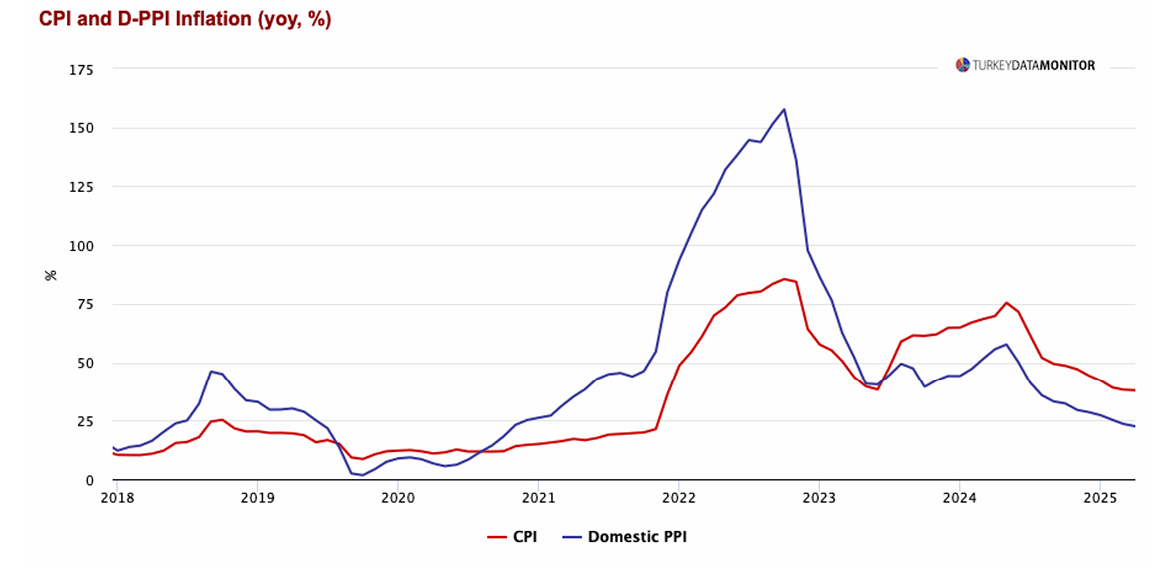

Fitch’s baseline scenario for Türkiye assumes sustainable GDP growth around 3.5% and a continued disinflation trend.

Kılınç described lower interest rates and progress on disinflation as the foundation for macroeconomic stability, but he also flagged ongoing policy risks:

“Monetary policy decisions, credit limits, and regulatory adjustments will be key risk factors to watch.”

AT1 Bond Issuances Strengthen Capital Buffers

Kılınç said Türkiye retains flexibility in accessing international debt markets, with many local banks turning to Additional Tier 1 (AT1) bond issuances to reinforce their capital structure.

He added that such issuances are becoming more common across the sector, and that domestic dynamics — rather than global pricing alone — now drive investor sentiment toward Turkish bank debt.

While these AT1 deals are viewed as positive for capital adequacy and investor confidence, Kılınç cautioned that risk premiums remain relatively high.