Higher inflation. Slower growth. Tightening financial conditions.

In recent weeks, Russia’s invasion of Ukraine has exacerbated global economic risks. There is a fourth element, however, that could make the mix combustible: the high debt of emerging markets and developing economies.

These economies account for about 40 percent of global GDP. On the eve of the war, many of them were already on shaky ground. Following up on a decade of rising debt, the COVID-19 crisis expanded total indebtedness to a 50-year high—the equivalent of more than 250 percent of government revenues. Close to 60 percent of the poorest countries were already in debt distress or at high risk of it. Debt-service burdens in middle-income countries were at 30-year highs. Oil prices were surging. And interest rates were rising across the world.

In such conditions, history shows, one more surprise is all it takes to touch off a crisis. The Ukraine war immediately darkened the outlook for many developing countries that are major commodity importers or highly dependent on tourism or remittances. Across Africa, for example, external borrowing costs are rising: bond spreads are up by an average of 20 basis points.

The calculus for countries for high debt, limited reserves, and payments coming up soon is suddenly very different: Sri Lanka, for example, opted last week to consider an International Monetary Fund-supported program in the face of a heavy debt service burden.

Over the next 12 months, as many as a dozen developing economies could prove unable to service their debt

That’s a large number, but it would not constitute a systemic global debt crisis—it would be nothing like the Latin American debt crisis of the 1980s, for example. It would be nothing like the 30-plus cases of unsustainable debt that prompted the establishment of the Heavily Indebted Poor Countries Initiative (HIPC) in the mid-1990s. Yet it would still be significant—the largest spate of debt crises in developing economies in a generation.

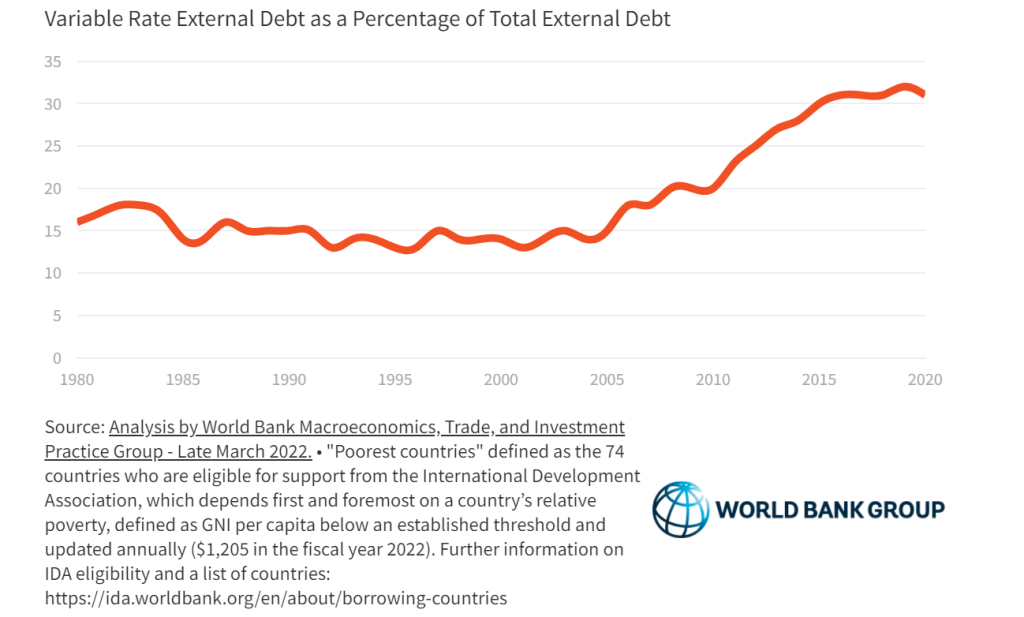

These crises, should they occur, would play out in a transformed landscape. Thirty years ago, developing economies owed most of their foreign debt to governments—official bilateral creditors—nearly all of whom were members of the Paris Club. Not so today: at the end of 2020, low- and middle-income economies owed five times as much to commercial creditors as they did to bilateral creditors. This year, of the nearly $53 billion that low-income countries will need to make in debt-service payments on their public and publicly guaranteed debt, just $5 billion will go to Paris Club creditors. Much of the debt of developing economies, moreover, now involves variable interest rates — meaning they could rise almost as suddenly as rates on credit-card debt.

The main global mechanisms available today to tackle debt crises weren’t designed for these conditions. They must be updated.

Fed Interest Rate Hikes Will Hurt Turkish Economy (And Other Emerging Markets) Badly

The G20 has played a crucial role in this process over the past two years. With the arrival of COVID-19, at the urging of the World Bank and the IMF, the G20 moved swiftly to set up the Debt Service Suspension Initiative (DSSI). The initiative brought together Paris Club members as well as non-members to provide about $13 billion in suspension of debt payments for nearly 50 countries. But that was a temporary safety net that expired at the end of 2021, just as the COVID-19 economic recovery had begun to run out of steam.

Following the DSSI, the G20 established the Common Framework for Debt Treatments beyond the DSSI. So far, just three countries have applied and progress on restructuring their debts has been slow. That sends exactly the wrong signal to other countries with unsustainable debt, many of which have refrained from seeking the relief precisely because of the slow progress: they fear applying to the Common Framework would cut off their access to private capital without restoring the flow of bilateral credit.

As a practical matter, the Common Framework is the only game in town—and it can and must be improved in time to provide meaningful relief to countries that need it. The World Bank and the IMF have offered a roadmap:

First, establish a clear timeline for what should happen when in process: the creditors committee, for example ought to be formed within six weeks.

Second, suspend—for the duration of the negotiations—debt-service payments to official creditors for all Common Framework applicants.

Third, assess the parameters and processes of the comparability of treatment and clarify the rules for its implementation.

And, fourth, expand the Common Framework’s eligibility requirements, which are currently limited to 73 of the poorest countries. They should be expanded to cover other highly indebted and vulnerable lower-middle-income countries as well.

For too long, the world has taken a tragically languorous approach to resolving debt crises in developing economies , delivering relief that is either too little or too late. It’s high time for a 21st century approach—one that involves pre-emption rather than reaction, one that prevents the crisis from erupting in the first place.

Follow our English language YouTube videos @ REAL TURKEY:

https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng