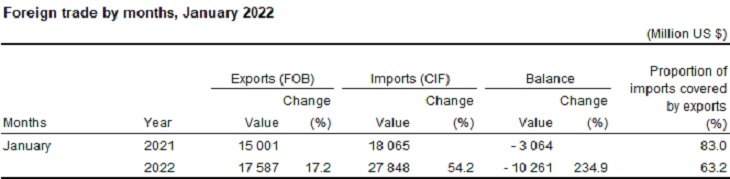

Turkish Statistical Institute announced in January 2022; exports were 17 billion 587 million dollars with a 17.2% increase and imports were 27 billion 848 million dollars with a 54.2% increase compared with January 2021.

Hence the trade deficit of 10.3 bn dollars corresponds to an alarming 235% yoy growth in foreign trade deficit.

In January 2022, seasonally and calendar adjusted exports decreased by 4.9% imports increased by 10.0% compared with previous month.

Exports, excluding energy products and non-monetary gold, were 16 billion 751 million dollars with a 19.6% increase in January 2022. Imports, excluding energy products and non-monetary gold, were 18 billion 413 million dollars with a 31.1% increase in January 2022. Foreign trade deficit, excluding energy products and non-monetary gold, was 1 billion 662 million dollars in January 2022.

Is the government’s current account surplus target possible?

Two main factors are behind the increase in Turkey’s foreign trade deficit. The first is the inevitable slowdown in the performance of the exports, due to rising inflation and slowing foreign demand. We will see this trend accelerating in the coming months as Turkey’s export growth normalizes after the pandemic. Of course, the shock of war inside Europe could also act as an accelerator to external demand.

On the other hand, Turkey’s energy import bill will continue to inflate given the spike of the oil price. During the first quarter of 2022, the trend of a 50% or more increase in imports will be permanent.

The January foreign trade figures are a harbinger of reality for the AKP’s economic management, which is pursuing the dream of achieving price stability through a current account surplus. While rising energy costs will drive up inflation, weaker-than-expected tourism revenues will be among the reasons for creating a current account deficit.

The government will face the consequences of implementing a dangerous economic policy. The calm provided by the $4-5 billion “unofficial” sales to keep TL stable in the wake of the Ukraine War, will leave its place to pressures on TL as Turkey’s CAD widens, Fed steps in with rate hikes and geopolitical risks remain elevated.

Ordinary Russian citizens will rein in holiday spending, accompanied by rapidly rising inflation and the loss of income generated by the currency depreciation. The limitations to move hard currency will add to this trend. From Ukraine, it is unrealistic to expect tourists. In this case, the $35 billion tourism revenue target of the government will fall short to a tune of USD 5-6 bn given that a part of the European originated tourists could as well refrain from Turkey holidays

Assuming the oil price at $100/ barrel throughout the year which will by itself add roughly USD 15-20 billion to the current account deficit, the CAD will also be fueled by weaker than expected tourism flows and slowing export growth.

In 2022 we will see Turkey’s current account deficit level rapidly doubling from the 2021 level of USD 14.9 billion towards USD 30-35 bn.