The debate around inflation is centre stage at present, with headline and PPI inflation soaring globally in response to a range of factors but including climate change/transition and Covid related supply disruptions. Views are, however, mixed as to whether the ongoing surge in inflation is likely to be permanent or transitory, and whether central banks need to react (if permanent) or can adopt a much more relaxed approach (“seeing though the inflation”) if transitory.

Generally DM central banks seem to be in the transitory camp, perhaps as a reflection of their experience of several decades now of low inflation or even grappling with the different challenges of deflation.

The reaction function of EM CBs is much more heterogeneous, depending I guess on their recent historical experience with inflation and perhaps also their political setting. A number – the CBR, CNB and BCB – are preemptively hiking, and aggressively at that. Others, like the SARB, appear willing to wait and see. I would put the CBRT in Turkey into a totally different unorthodox camp, actually cutting interest rates in the face of very high and rising inflation.

To set out my own stall at the outset, I am strongly of the view that we experiencing a paradigm shift on inflation – and we are facing a perfect storm, that presents the biggest risk of a sustained and extended period of inflation, not seen since the 1970s.

But first perhaps it is worth setting out the case made by the “inflation is transitory” camp, which will help me better then attempt to debunk this view.

I guess the basis of the “inflation is transitory” argument is that while supply chain disruptions caused by Covid will spike inflation in the short term, all the forces that drove inflation lower, and indeed very low, through the 1990s to the period immediately before Covid, remain intact and will inevitably force inflation to mean revert to very low levels again. So think here of very powerful forces, including globalisation, free trade, and the application of technology to supply chains and markets. They would add that Covid has seen millions of people left unemployed, or temporarily parked outside of the labour force though various furlough schemes, but as wages begin to rise again they will be quickly encouraged back into work, capping any pressure on wages and core inflation. They would also argue that global output is close to pre pandemic levels, but in the US at least is being produced by much fewer people, hence already technology is doing its thing to keep the supply curve moving out right.

A mea culpa herein perhaps that there have been many boys (inflaionistas) that cried wolf on the inflation front in recent years, but all have been disappointed.

I would though argue that something is very different this time around

But before going there I think it is perhaps worth going back to the drivers for the era of low inflation, the dynamics therein, to perhaps understand why things might be different this time around.

And I think to understand the victory over inflation achieved in the 30 years to Covid, it’s important to go back to the 1970s. Arguably this was an era of peak inflation, as the decade marked a peak in Unionisation in Developed Markets. Labour had pricing power, and arguably oil producers found similar pricing powers with the formation of OPEC after the Middle East wars of the same decade. High inflation was jeapordising global growth, returns on capital, and arguably political cohesion and stability in the West – see the wave of strikes and industrial unrest in the UK in the 1970s. The political counter reaction saw the rise of leaders such as Thatcher and Reagan. The solutions rolled out by these leaders were seen as globalisation to break Union power, and free trade, plus deregulation which I also see as part of the freer trade agenda. Western multinationals were encouraged to move production facilities to other global locations, and free trade enabled product produced in these locations to be exported back to DMs, cheaply and significantly tariff/NTB free to developed markets. Multinationals were able to exploit cheap labour in EMs, where restrictive labour practices were limited or non existent. Cheap EM labour thus undermined the hold of Unions in Developed Markets, and drove more flexible labour market practices even in DMs. Labour globally lost pricing power. Technology was applied to ensure optimal production chains, with output produced to maximise economies of scale and taking full advantage of cheap labour, and low/non existent ESG standards in EMs.

Technology aided this process not only by optimising efficiencies in supply chains, but through the on set of the internet, which ensured almost perfect global price discovery and near perfect global competition.

Consumers in DMs benefited from cheap consumer imports, and low inflation which arguably helped cap wage price pressures. But the bulk of mass skilled jobs in manufacturing were exported from DM to EM. Capital in EM benefitted, and a small elite of value adding highly skilled workers in DM did well – they had the skills still to command a wage premium. The bulk of former unionised labour in DM though became largely unskilled, commoditised, un-unionised, and largely service sector in lowly paid jobs. Again their pricing power collapsed, and this drove great inequality in DM – ultimately the harbinger of exclusive growth, Rust Belts, the Northern Wall, et al. More of the latter later.

It’s probably worth noting here that alongside globalisation, free trade, and technology, the other leg of this process was provided by ideology. This was the idea that unfettered free markets were the ideal, and free markets would inevitably see democracy flourish globally. This is important as all this largely coincided with the fall of Communism in Eastern Europe from 1989, and then the opening up of China. The assumption was that it was fine to allow relocation of productive assets from the West to Communist China and Russia in transition by then et al, as particularly in the case of China, it would promote the evolution of free markets and a capitalist class which would inevitably see the demise of the remnants of Communism: “they would become like us”. This was a huge error with hindsight, but which I will come back to later, as it is now a risk of being a factor to force inflation higher. But sure, in the short term, this move of Western capital and manufacturing capacity into Emerging Europe, and China, but also India and other Emerging Markets released a huge latent mass of cheap labour which helped drive inflation lower over the past 20-30 years.

So why do I think the current spike higher in inflation will prove long(er) lasting?

Inflation is likely to prove long lasting as a perfect storm is brewing for inflation globally, with a range of factors all coming together at the same time to shock the system, and which are eroding the dominance of forces of disinflation seen over the past 30 years.

First, as even the transitory crew would agree Covid is causing huge disruptions to finely calibrated supply chains, many of which are interconnected. Prices are rising and fast, the data is clear. But will it prove long lasting?

The transitory crew would argue that market forces and technology will quickly see markets and prices settle, and much lower.

I would counter that it’s just the shear extent of global disruption and the interconnected nature of global supply chains which suggest such supply shocks will more likely last many many months, if not years. This already seems to be proving to be the case. A year on from the first price shocks and prices are still on the up. Transitory already feels like proverbially asking the length of a piece of string.

Second, and related, Covid seems to be changing a whole range of demand and supply factors, and shifting both curves across multiple industries and product chains around as never seen before since perhaps the 1970s.

In response to Covid we are changing where and how we work and live, and what and where we consume. Markets, perhaps even industries, and companies are dying and being born during this period. It’s a period of intense disruption. The cards are all being thrown on the floor, and it will take time to pick them back up and reorder the pack. But during this time we are seeing intense shortages and surpluses of products. High and low prices. But shortage seems to be dominant theme.

Economic theory here – the Cobweb Theorem or Hog Cycle – would suggest suggests a long period of distruption, and markets might take time to clear and especially where supply curves are more elastic than those of demand.

Third, Covid hit as the world grappled with the challenges of climate change and efforts at climate transition.

Climate change has brought challenging agroclimatic conditions in many parts of the globe, causing disruptions to agricultural production and food supply. Food prices are near historical highs.

Climate transition has been mismanaged (we are all guilty) and this winter we have seen the impacts of that in European gas and energy markets. Lack of planning and forethought has seen carbon production taken off line, while renewables lack capacity to sustain any shortfall year around. Huge rises in oil, coal and gas prices have resulted. The immediate challenges of climate change suggests that the carbon transition will be disruptive, and energy shortages could prove longer lasting, not helped by geopolitics (see below).

Fourth, and linked to the carbon transition, ESG has exploded. Inevitably this challenges the free market, unfettered globalisation agenda above. ESG means that Western governments, companies and consumers are no longer willing to look the other way when globalisation means that products produced in low wage, low regulation offshore locations. See now all the focus on cotton is produced for the Western rag trade by Xighur in China.

The hope is that ESG will raise standards globally, but likely will increase costs across the board, shifting supply curves up and to the left. Arguably the carbon transition will do something similar until a critical mass of investment in renewables is reached to fully take the strain from carbon.

Fifth, the rise of populist politics, mixed in with geopolitical competition and tensions means that the trend is no longer one towards ever freer markets, but instead to greater trade autarky. Governments in developed markets are laser focused on delivering inclusive growth, to “level up” society and to counter the tendency towards centrifugal forces playing out in politics – the rise of far left and far right populists. This means more regulation, a desire to onshore more production and use tariffs and non tariff barriers and tax policy to deliver on this. Covid has arguably accelerated this process, as supply chains have proven strategic. Countries want to ensure domestic supply of critical products like medicines or healthcare equipment, food, energy, microchips. The realisation is dawning that globalisation and multinationals might be working against national interests. But this means more localised production, reduced use of global supply chains and inevitably less ability to play on global economies of scale. Again it likely means supply curves shift up and the left – less output at higher prices.

The geo-politics of inflation

Sixth, and back to geopolitics. We cannot ignore that the US and China are in a battle for hegemony. The US is realising that globalisation has not resulted in China becoming “more like us”, instead state capitalism has resulted and prospered to the point that it is challenging US global hegemony and exceptionalism. The US response has been tariffs and regulation to restrict trade. China has retaliated. It’s hard to see this trend reversing when both now see the relationship being based on a zero sum agenda. Both want to see the other fail. Other countries are having to choose which side they are on, but the result again is likely to be less globalisation, less free trade, more regulation, tariffs, and higher costs of production all around.

And the battle for hegemony is not only between China and the US, but also between Russia and the West. Similarly, globalisation did not make Russia “more like us” but resulted in the victory by an autocratic and kleptocratic regime which appear set on the destruction of the Western Liberal Democratic model – if Russia has indeed interfered in Western elections, and is using kleptocracy to corrupt our systems from within. But Russia seems to have felt so aggrieved at the state of its relations with the West that it has sought this winter to use the energy card against Europe through the gas crisis in Europe. Let’s not forget that the Soviet Union never did this through the Cold War, or did Russia in the period to this year.

The energy blackmail

But Russia does seem to have acted to limit supply into storage through the summer, to leave Europe short of gas this winter and to have had a major contributory effect towards high gas prices this winter. Perhaps this is because it ultimately sees the carbon transition as killing the golden goose of energy exports and its time is now to use leverage for strategic gains, over Ukraine. But net net, Russia’s actions seem to have pushed energy prices higher this winter, and it’s hard to see a reversal in this strategy. Indeed, recent years have seen Russia ally with the OPEC oil price cartel (forming OPEC+) to keep oil and energy prices higher. Again it is hard to see this strategy changing. Energy prices look set to stay higher longer.

Geo-political competition rises across the globe

Competition is also not exclusive to the West versus China, but even within the West we have had populism result in Brexit in the UK, and trade barriers (fish wars between the UK and France) erected again even between allies and supposed friends. Brexit might not be the end of centrifugal forces in the EU – watch therein relations between Brussels and the likes of Poland, Hungary and even Slovenia.

Covid-19 causes paradigm shift in economic policy

Seventh, the policy response to Covid has been exceptional, even extraordinary. Central bank balance sheets which had already been greatly expanded because of the GFC have been further inflated. Fiscal policy has been massively loosened. Both are being very slow to be reined in. In many emerging markets, particularly, in Emerging Europe, labour markets were already very tight before Covid hit, output has recovered rapidly, already recovering losses from Covid, but fiscal policy remains hugely expansionary, while monetary policy, albeit tightened somewhat, remains very lose, and much looser still then pre Covid – most central banks are still running negative real interest rates. We are celebrating the fact that many EM central banks are now hiking policy rates but they remain far below historical levels, even though inflation is again approaching highs of the past.

And let’s not forget that in EMs, populations still have recent memory of inflation, and it’s notable to see inflationary expectations rise rapidly – in Russia and Turkey, for example, household expectation surveys shows inflation running twice headline numbers – and actually this makes more benign central bank and market forecasts appear obsolete.

Emerging Markets: The Dawn Of A Lost Decade | Real Turkey

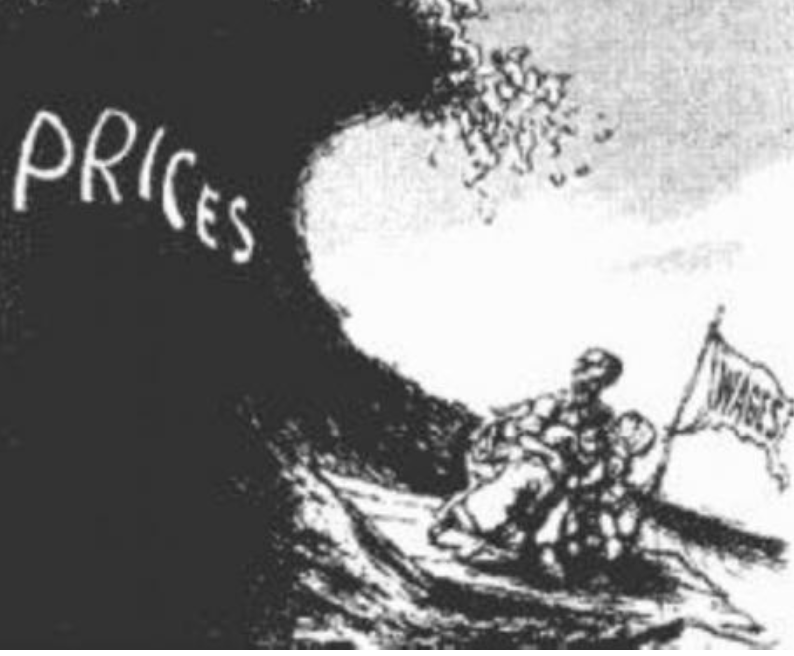

Eighth, but linked this time around to the policy response to inflation, group think in DM central banks that the current inflation splurge is transitory appears to be based on conclusions drawn only in recent history but which seems to have no relevance to the new environment post Covid. In particular, here I would highlight with little experience of inflation over the past thirty years, it’s unclear how consumers, or workers will react. Why should DM consumers be different to those in EM in terms of setting inflationary expectations? Maybe they will prove more risk averse and inflation focused. Indeed, central bankers might view inflation as transitory but workers are unlikely to take the same sanguine view when they see inflation eating away at their standards of living.

DM central bankers seem to be still in the post GFC environment, and also perhaps still of the mindset that growth and jobs have to be prioritised at all cost so as to head off the risk of populist backlash – countering risks of future Donald Trump style events. But this ignores the fact that while weak growth impacts a relatively small section of the population through unemployment, high inflation impacts the bulk of the population and the poor both in and out of work. Inflation is highly regressive. Policies rolled out, post GFC, to keep growth and employment high, have moreover proven to be highly regressive. QE has boosted asset prices, and the wealth of the middle and upper classes, not the working classes. It has increased inquality – QE, rate cuts and fiscal stimulus in response to Covid has lined the pockets of billionaires.

How Bad is Fed Taper for Turkish Assets?

Inflation is eating away at the living standards of the poor, the bulk of the electorate. How long before central bankers in DM realise this? By then they are likely to be way behind the curve and will need then to play aggressive catch up with large and likely then destabilising interest rate hikes.

So likely DM monetary policy will remain looser for longer, and although EM central banks appear to be waking up sooner to smell the coffee, the reality is a decade of QE, or cheap DM money, is that it has seen resource and credit mispricing globally, and acted to put less pressure on EMs to drive on with much needed structural reform. Herein empirical evidence suggests that the pace of TFP growth in EM has slowed since the GFC and the onset of QE. That means EM is producing goods less efficiently in effect, and at a higher cost. And the longer QE remains in place through Covid TFP in EM will further lag. The result is again supply curves move up and to the left.

On this note, tell me where in EM we are seeing a country push on with successful structural reform. Looking at the big EMs, I don’t see it in the likes of Russia, Turkey, Brazil, Argentina, South Africa, Nigeria, Indonesia, Mexico. I see the reverse. Perhaps in Emerging Europe, in the likes of Central Europe, albeit rule of law is in question even in the likes of Poland and Hungary now.

In conclusion, I would argue that the case for inflation to be sustained at higher levels for longer is compelling. We are living through a new paradigm, a shift occurring in so many plates but working to the same likely effect, higher prices.

But I would love to hear your views.

** Please note that any views expressed herein are those of the author as of the date of publication and are subject to change at any time due to market or economic conditions. The views expressed do not reflect the opinions of all portfolio managers at BlueBay, or the views of the firm as a whole. In addition, these conclusions are speculative in nature, may not come to pass and are not intended to predict the future of any specific investment. No representation or warranty can be given with respect to the accuracy or completeness of the information. Charts and graphs provided herein are for illustrative purposes only.

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng