Recommendation summary

Most consumer names we cover are holding up well in terms of growth and are defending/growing their profitability

Growth remains strong for 3Q with expansion in EBITDA margins, but opex challenges are gradually increasing

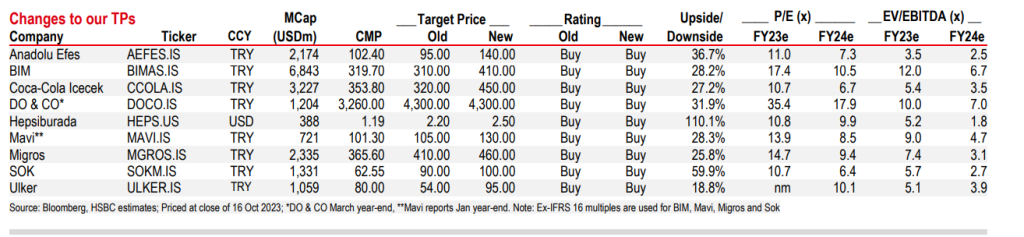

We prefer BIM and Mavi, both rated Buy; reiterate Buy ratings on our other consumer names, increase TPs for all names except DO&CO

Holding up well

We expect top-line growth rates for our consumer coverage names to be in line with inflation trends as incremental growth starts to taper off under a tightening liquidity environment. The current high inflation environment is impacting larger ticket items (ie, cars, housing) but is overall neutral for our covered staples and discretionary names in Türkiye, in the short term. Consumers are showing some resilience on small ticket spending, supported by the minimum wage hike in July 2023. However, we expect pressure to build at the opex level due to higher wages and increasing fuel prices, likely reflected later in 2023. Most consumer names we cover are holding up well in terms of growth and are defending or growing their profitability; the outlook for 2024 could change depending on wage increases and the severity of the consumer pullback.

Volatility and concerns on consumer health are likely to continue as the economy navigates a challenging return to conventional economic policy. In 3Q23, we see stronger performance from BIM and CCI.

We prefer BIM and Mavi

We are positive on our consumer coverage in Türkiye due to their resilience to the challenging macro backdrop. We do not see significant changes in the structural and long-term growth outlook, as most of the companies are able to drive better pricing and control their costs. Under the tightening liquidity situation, we think investors are likely to focus on companies with strong fundamentals, stable cash flows and those that have a competitive advantage. We like BIM given its strong market positioning in the discount space and its diversification strategy which should enable it to capture higher market share over the long term.

We also like Mavi given its growing brand image and the strong competitive advantage it holds in Türkiye. We reiterate our Buy ratings on all other consumer stocks under our coverage based on valuation, with changes in TPs highlighted below.

Excerpt from HSBC report titled “Turkish consumers – Holding Up Well”

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/