Despite skyrocketing food and energy prices, Covid-19 coming back from its presumed demise time after time, and the real threat of tightening by reserve money central banks, IMF and World Bank draw a rosy picture of the world in 2022. Both supra-nationals predict moderating growth and inflation.

Their recent reports do pay homage to downside risk, but these don’t seem to affect the rather optimistic base-case scenario. (We have only read the excerpts provided by IMF and WB, retaining our right to change our view once the full texts are available to public.)

On the other hand, investment banks and financial experts are increasingly becoming pessimistic about 2022 outlook, with stagflation preoccupying global money managers.

Danske’s is the first report (among those registering on our screen) to explicitly point out 5 major risks to the benign 2022 scenario.

Here is what the analyst wrote for 2022

Five reasons we see rising downside risks to growth

Following a very strong rebound from the COVID crisis we see rising downside risks to global growth over the coming quarters.

Below we briefly go through five factors that have developed worse than expected over the past months.

- Chinese growth risks have increased. The Evergrande crisis is set to lead to weaker Chinese performance and we have revised down our GDP forecast for this year to 8.0% (from 8.5%) and to 4.5% in 2022 (from 5.0%), see China Macro Monitor – Growth revised lower as property crisis to linger into 2022, 4 October 2021.

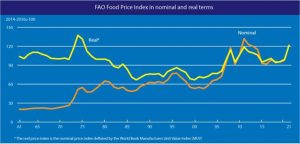

- An energy ‘crisis’ is eroding purchasing power. The sharp rise in gas and electricity prices we witness in Europe will lead to a longer period of high inflation in the euro area. If current levels of gas and electricity last throughout the winter, it could add around 1 percentage point to Euro inflation, which will erode purchasing power among consumers. A rise in inflation basically works as a tax on consumption.

Oil prices have also increased more than expected, which will also delay the decline in US inflation, eroding the purchasing power of the US consumers.

- Covid herd immunity is not reached ahead of winter. A key assumption for our forecast has been that herd immunity would be reached ahead of the winter season, where contagion tends to increase. However, in the US it looks like only around 60% of the population will be fully vaccinated and in Europe the number is around 75%.

With the more contagious delta variant most estimates of herd immunity are around 80-90% and we could thus very well see new covid waves once the cold weather hits.

WATCH: Emerging Markets: The Dawn Of A Lost Decade | Real Turkey

While we don’t expect this to trigger new lockdowns it could still hit not least service consumption as unvaccinated people are likely to go less out during a covid wave.

- Higher inflation is tying policy makers’ hands. Under normal circumstances central banks would delay policy tightening amid a slowdown. However, the current inflation pressures will likely require that central banks proceed with tightening plans and we expect the bar to be high for the Fed to delay tapering. Given the stagflationary environment, there is simply less room for central banks to support growth.

WATCH: Clash of Civilizations Reformatting World Economy | Real Turkey

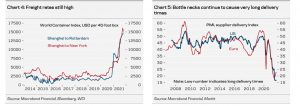

- Supply chain disruptions continue. Bottle necks throughout the supply chains remain unresolved. In many Asian countries covid waves have disrupted production and now that lockdowns are eased, many migrant workers in factories are returning back to their villages leaving labor shortages intact, see for example this article on the issue in Vietnam. Shortages of microchips also continue to be an issue for the car industry.

Editor’s Comment

PATurkey is mostly about Turkish affairs, but we also cover EM and the global economy for the simple reason that Turkey is a medium-size price taker economy fully integrated to the global goods and financial markets. We shall soon post an article on how Turkey’s economic fortunes will dim in Stagflation World future.

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng