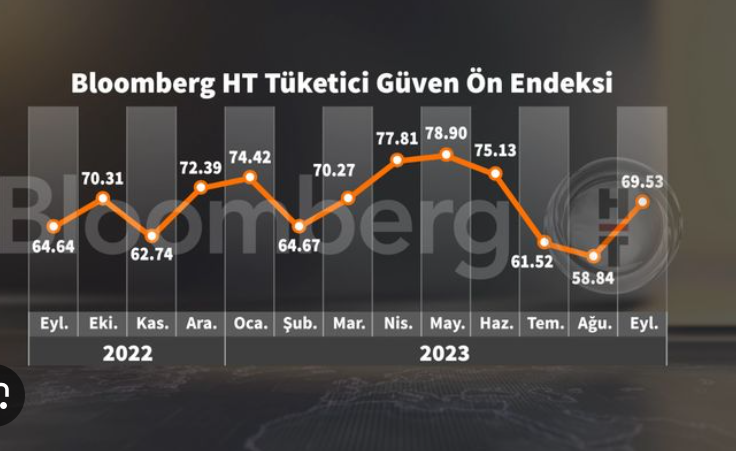

On Monday, private financial broadcaster BloombergHT published its September preliminary consumer survey, which is even older than the stats agency Turkstat’s series. The headline jumped by 11 percentage points, after testing historic lows in July and August. This is bad news for Turkey’s fledgling economic stability program, because the economy is too hot going into winter months, when inflation and current account deficits could lead to drastic political and balance of payments shocks.

BloombergHT consumer confidence survey, September preliminary, in Turkish

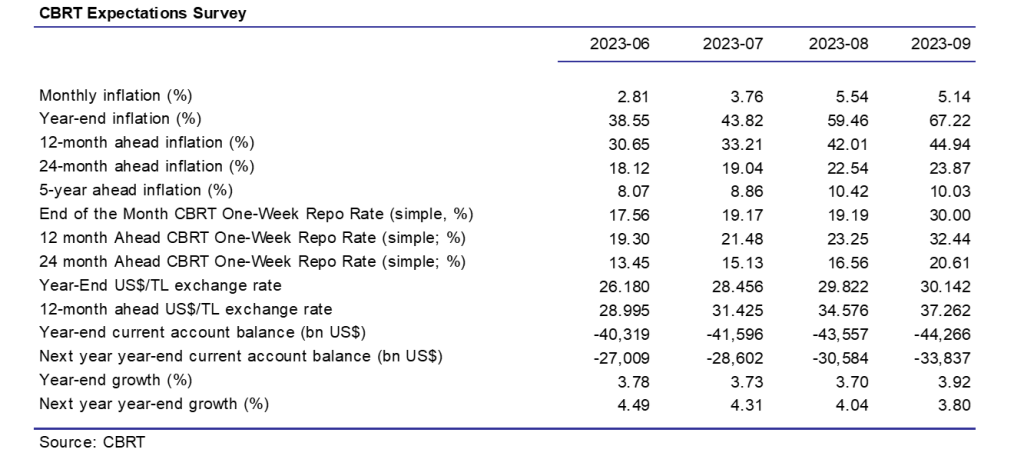

According to Central Bank of Turkey’s (CBRT) September expectations survey, 12 and 24 mth ahead inflation forecasts exceed 66% and 44%, respectively. The CAD forecast is $44 bn for YE2023, with next 12 months at $33.5 bn. Worth noting that these forecasts have all increased substantially vis-a-vis the previous survey. Also worth noting is that CBRT’S hand-picked participants always underestimate these magnitudes.

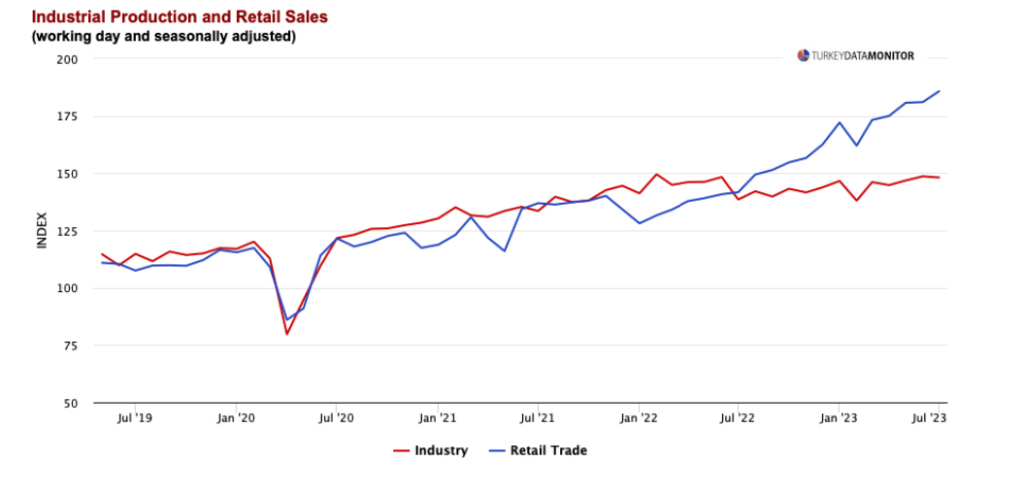

Rising consumer confidence means more domestic spending, which inevitably spills into inflation and CAD. The news gets worse: the rise in private spending intentions is not matched by domestic production. The chart below, from my team, Global Source Partners TURKEY, illustrates the yawning gap between production and spending, which means each TL of private consumption will have a higher impact on inflation and CAD.

At the end of the first three months of the tenure of the new economics trio (VP Cevdet Yilmaz, economy czar Mehmet Simsek and CBRT governor Hafize Gaye Erkan), no progress has been achieved in easing Turkey’s economic imbalances despite draconian tax hikes the value of which are estimated at 4% of GDP, a massive credit crunch and modest increases in policy rate.

My team estimates that Turkey’s external financing need is $50 bn in the next six months. In addition to that the economy trio wisely decided to wind down the costly and financially destabilizing FX-protected deposit scheme (Also called KKM in English articles), which has accumulated quasi-dollar deposits of $120 bn. CBRT doesn’t have that kind of FX reserves to cover external financing AND savers migrating from FX protected to straight FX deposits, which could add up to $30 bn to spot FX demand over the next six months.

A winter when rising energy prices are stoking CAD, CBRT reserves falling and rampant inflation forcing a faster rate of exchange rate depreciation is a recipe for crisis. Mr. Erdogan desperately wants to win March 2024 local elections, which means there is a ceiling how high monetary tightening can go. Moreover, judging by July-August budget figures, which saw the accumulated deficit dropping from 6% of estimated GDP to 3%, the Ministry of Finance is preserving fire power to feed the voters in the 1st quarter of 2024, which will add fuel to the bonfire of inflation and CAD.

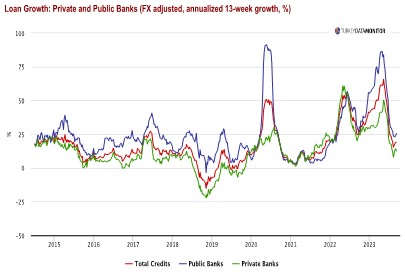

Mind you, I’m not predicting a crisis. While monetary tightening through the interest rate channel is modest, the CBRT-introduced credit squeeze is gigantic. Look at the chart below. CBRT’s closely watched loan trend predictor, 13 week moving average annualized loan growth (FX adjusted) has dropped from 70% before elections to 20% or so.

There is a strong negative correlation between credit impulse in the summer and economic activity in the winter. It is conceivable that credit policy will be tight enough to moderate domestic demand and tame soaring inflation and CAD. However as I have said, Erdogan will probably not want a visible growth slow-down on account of upcoming local elections.

A seldom talked-about success of the current economic program is rising deposit rates on TL, which could seduce residents to switch from KKM to TL deposits, but TL deposit rates will have to rise to at least 70% from the current 45% to ensure such an outcome. This is not unachievable, but the cost will be a complete stand-still in loans and rising bankruptcies.

The only way Turkey can spend her way through winter, as Erdogan wishes and not experience a currency shock is Mehmet Simsek attracting large amount of foreign financial investment. This is why he will be touring the world to drum up support for the economic program. In my tentative and humble estimate, Turkey needs to attract $25 bn of “hot money”, or UAE must deliver on its promise of two long-term loans totaling $11.5 before elections for comfort.

Can this be done? If global risk appetite for EM rises, perhaps; at least I won’t rule it out. But, it is always risky to rely on the kindness of foreigners, as the saying goes.

By Atilla Yesilada

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: https://www.facebook.com/realturkeychannel