Production Slowdown Deepens as Demand Weakens in Türkiye

Turkish steel production

Turkish steel production

By Güldem Atabay

Summary: March 2026 data point to a clear loss of momentum in Türkiye’s economy, with weakening demand, rising cost pressures, and deteriorating confidence indicators. While some production indicators remain resilient, underlying trends suggest growing fragility and rising stagflation risks.

SAMEKS Signals Persistent Weakness in Economic Activity

March 2026 SAMEKS data indicate that Türkiye’s economic slowdown is becoming more entrenched, particularly on the demand side.

The seasonally and calendar-adjusted Composite Index remained at 49.1, below the critical 50 threshold, signaling continued contraction. This suggests that the economy is not only slowing but increasingly settling into a prolonged period of weak growth.

The data confirm that economic activity is entering a demand-driven slowdown phase, accompanied by ongoing imbalances between sectors—raising concerns about the sustainability of the current growth composition.

SAMEKS PMI Signals Slowdown as Turkey’s Economic Momentum Weakens before the War

Industry Holds Up—But Cracks Are Emerging

One of the most striking aspects of the data is the divergence between industry and services.

The industrial SAMEKS index remained above the threshold at 50.7, but the sharp monthly decline of 5 points signals a clear loss of momentum. Beneath this relative resilience, deeper weaknesses are becoming visible.

- The production sub-index showed only a limited increase (48.6)

- New orders fell sharply by 10.6 points to 49.5, indicating weakening demand

- Input purchases dropped dramatically by 24.8 points, pointing to deteriorating expectations

Meanwhile, rising inventories and improved delivery times suggest that firms are shifting toward more cautious production and stock management strategies.

Employment remains relatively strong at 61.6, but the sustainability of labor demand in the face of weakening orders is increasingly uncertain.

Services Sector Remains Fragile

The services sector presents a more balanced but still weak outlook.

While business volume improved slightly to 48.1, it remains below the expansion threshold. Declines in input purchases and continued weakness in employment—at 47.8—highlight ongoing fragility.

Overall, the data suggest a clear divergence:

- Production and employment show relative stability

- Demand indicators continue to deteriorate

PMI Confirms Broad-Based Slowdown

March PMI data reinforce the picture of a weakening economy.

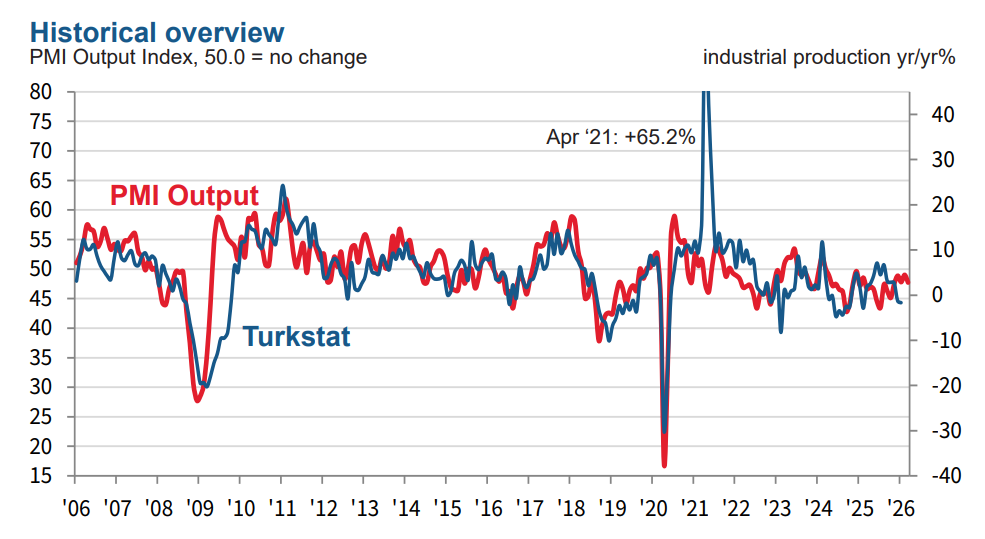

The manufacturing PMI fell from 49.3 in February to 47.9 in March—its lowest level in five months—indicating a renewed contraction in industrial activity.

The key driver is demand:

- Both domestic and export orders are weakening simultaneously

- This marks a critical shift, as external demand had previously helped offset domestic weakness

Firms increasingly attribute this slowdown to geopolitical uncertainty, particularly the ongoing conflict in the Middle East, which is driving both uncertainty and cost increases.

Cost Pressures and Stagflation Risks

The second major theme is rising cost inflation.

According to PMI data:

- Input costs rose at the fastest pace in 23 months

- Output prices increased at the fastest rate in 25 months

Energy, logistics, and raw material costs are the primary drivers.

This creates a classic “cost-push inflation + demand contraction” dynamic—one of the most challenging environments for policymakers.

Real Economy Impact: Production and Jobs Under Pressure

Weak demand and rising costs are now translating into real economic contraction.

- Production decline in March was among the sharpest since November 2025

- Employment recorded its steepest drop in six months

This indicates that the slowdown is no longer limited to expectations—it is now clearly visible in both output and labor markets.

Supply Chain Disruptions Add to Fragility

Supply-side constraints are further complicating the outlook.

Delivery times have lengthened significantly, reflecting disruptions in logistics and supply chains linked to geopolitical tensions.

This adds upward pressure on costs while making production planning more difficult.

SAMEKS vs PMI: A Timing Difference

At first glance, SAMEKS and PMI may appear contradictory—industry remains above 50 in SAMEKS, while PMI signals contraction.

However, this reflects methodological differences:

- PMI is more forward-looking, driven by orders and expectations

- SAMEKS includes broader and partially lagging indicators

As a result, SAMEKS may not yet fully reflect the deterioration captured by PMI.

Taken together, both datasets point to the same conclusion:

Türkiye’s economy is entering a period of slower growth with rising stagflation risks.

Sharp Drop in Consumer Confidence

Poll Shows Confidence in Turkey’s Economic Management Stuck at 27%

March also saw a significant deterioration in consumer sentiment.

The Bloomberg HT Consumer Confidence Index fell sharply from 76 to 68, signaling a widespread and deepening loss of confidence.

Subcomponents reveal a troubling picture:

- Perceptions of current economic conditions have worsened

- Expectations for the future have deteriorated sharply

- The Expectations Index recorded a double-digit decline

Most notably, the Consumption Tendency Index dropped from 83.8 to 70.3, indicating a rapid decline in willingness to make major purchases such as cars and housing.

Demand Weakness Set to Intensify

The underlying drivers of this deterioration are clear:

- Geopolitical uncertainty, particularly the Middle East conflict

- Persistent inflation, eroding purchasing power

- Rising unemployment expectations, weakening household confidence

As expectations worsen, consumers are increasingly postponing spending and shifting toward precautionary savings.

This suggests that domestic demand—already weak—is likely to slow further in the coming months.

Conclusion: A Turning Point Toward Slower Growth

The latest data paint a consistent picture:

Türkiye’s economy is entering a phase of synchronized demand contraction, rising costs, and weakening confidence.

While parts of the industrial sector remain relatively resilient, the broader trend points to:

- Slowing growth momentum

- Increasing stagflation risks

- A more fragile economic outlook

The key challenge ahead will be managing this complex environment without further undermining growth or fueling inflation.

Related articles

+61K Turkish shop owners went bankrupt in 2021

Economic Crisis in Turkey Named Top Concern: Report

ANALYSIS: Turkish Industrial Production Sustains Strong Annual Growth on Low Base Effect