Global Bankruptcies Slow, but Türkiye Diverges: A Hidden Crisis Deepens

bankruptcy

bankruptcy

By Erol Tasdelen, banking consultant and ParaAnaliz.com columnist

While global bankruptcy growth is moderating, Türkiye is moving in the opposite direction. A sharp rise in corporate failures—up 29%—signals not a typical insolvency cycle but a deeper structural strain in the real economy. Analysts warn that what appears as stability may in fact be a fragile system sustained by credit, with risks building beneath the surface.

The latest Global Bankruptcy Report by Dun & Bradstreet suggests that the pace of corporate failures worldwide is slowing. After a 15% increase in 2024, global bankruptcies rose by just 7% in 2025. At first glance, this points to an economy that is cooling but not collapsing.

Türkiye, however, tells a different story.

Türkiye Breaks Away from the Global Trend

While the global economy appears to be stabilizing, Türkiye is experiencing a sharp deterioration in corporate balance sheets. Business bankruptcies have surged by 29%, a figure that goes beyond cyclical stress and reflects deeper systemic pressures.

This is not a conventional wave of insolvencies. Instead, it signals a broader breakdown in financial conditions across the real sector, driven by:

- Cash flow disruptions

- Tightening access to financing

- Pressure from high interest rates, currency volatility, and weak demand

Many companies are still operational, but their financial foundations are increasingly fragile.

The Rise of “Living but Dead” Balance Sheets

A growing number of Turkish firms are not formally bankrupt, yet they are no longer financially viable. These companies continue to operate through:

- Rolling over bank loans

- Extending payment terms

- Relying heavily on supplier credit

This phenomenon can be described as “living but dead” balance sheets—firms that survive only through continuous external support.

As long as liquidity remains available, these companies can stay afloat. However, any disruption to this flow could trigger a rapid and widespread collapse.

Policy Trade-Off: Disinflation vs. Corporate Survival

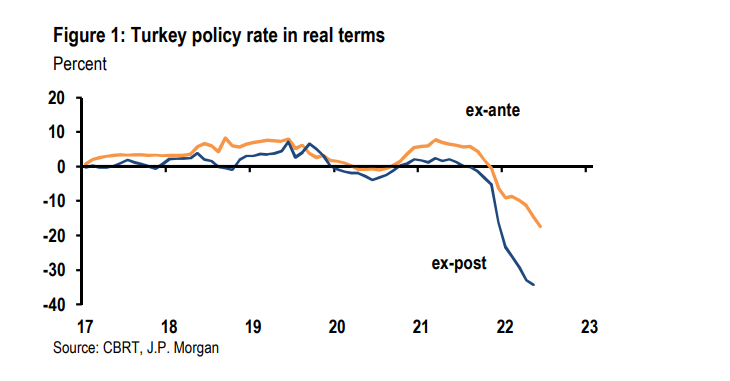

Türkiye’s current economic model is centered on reducing inflation by suppressing domestic demand. In theory, this approach is consistent with orthodox stabilization policies.

In practice, however, the consequences have been severe for the real sector:

- Demand has weakened

- Financing costs have surged

- Producers are under increasing strain

As a result, companies are weakening faster than inflation is declining. This raises a critical policy question: how much pressure can the real sector تحمل in the pursuit of price stability?

Concordat Filings Signal Deeper Stress

The recent surge in concordat (debt restructuring) applications is another warning sign. Traditionally used as a tool for corporate recovery, concordat is increasingly being used as a mechanism to delay inevitable defaults.

Many firms are not seeking restructuring to resolve their problems, but rather to buy time.

This suggests that the issue is not temporary but structural.

Banking Sector: Risks Building Quietly

On the surface, Türkiye’s banking system appears resilient. However, underlying indicators point to growing stress:

- Loans under close monitoring are increasing

- Restructuring activity is rising

- Collection periods are lengthening

While a full-blown banking crisis has not yet emerged, risks are accumulating. Historically, stress in the banking sector tends to materialize with a delay, often after vulnerabilities have built up over time.

Why the Global Context Matters

The divergence between global and Turkish trends is significant. While bankruptcy growth is slowing worldwide, it is accelerating in Türkiye.

This indicates that the country’s challenges are not primarily driven by external conditions, but by domestic dynamics.

Under similar global circumstances:

- Some economies are stabilizing

- Türkiye is becoming more constrained

This reinforces the view that the الأزمة is largely homegrown.

The Risk of a “Sudden Stop”

Perhaps the most critical risk facing the Turkish economy is the possibility of a sudden stop—a scenario in which economic activity abruptly stalls.

In such a case:

- Production could halt

- Payments could freeze

- Credit flows could dry up

Leading indicators of such a scenario are already visible:

- Rising bankruptcy figures

- Increasing concordat filings

- Deteriorating cash flows

Türkiye may already be entering this dangerous phase.

Conclusion: Not a Crisis—Yet

It would be misleading to describe the current situation as a traditional economic crisis. Instead, Türkiye is experiencing:

- A prolonged period of financial compression

- Silent erosion of corporate balance sheets

- A controlled economic slowdown

However, if this process continues unchecked, control may be lost.

The key question now is whether this tightening phase can be managed—or whether it will evolve into a chain reaction of corporate failures.

The answer will depend not only on monetary policy, but also on how much priority is given to sustaining the real sector.

Related articles

OPINION: Powell affair shows the US is devolving into a Greater Turkiye

Dr Özge Öner: The Economic Cost Will Become More Visible — and Harsher — in 2026

JP Morgan: Turkey: the CBRT shows no intention of tightening its policy