Will Turkey face a devaluation? Experts say a sharp devaluation is unlikely in the near term — but risks remain

tl1

tl1

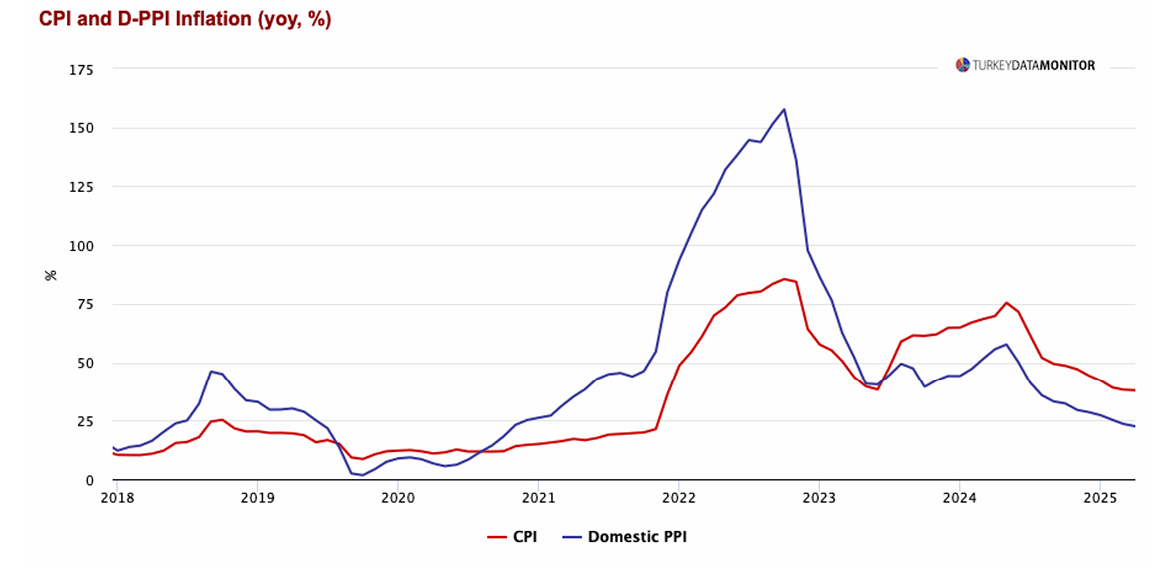

As the lira trades around ₺41.3 to the dollar and about ₺49 to the euro, debate is intensifying over whether Turkey faces a renewed, sharp devaluation. High-profile warnings from abroad — most recently by Robin Brooks, chief economist at the Brookings Institution — have added fuel to the conversation. Yet Turkish market and policy analysts say an outright, engineered devaluation is unlikely in the coming months. Instead, they point to a more nuanced outlook: gradual depreciation driven by policy choices and market sentiment, with episodic volatility tied to politics and external pressures.

Below we summarise the arguments, the key data points, and the views of Turkish and international experts on how likely a full-blown devaluation is — and what would have to change for that probability to rise.

Robin Brooks’s warning: “Inevitable” devaluation?

Robin Brooks, the internationally known chief economist at the Washington-based Brookings Institution, caused headlines when he argued that Turkey’s policy mix has left it structurally exposed to currency crises and on a path that could make devaluation “inevitable.” Brooks’ critique focuses on Turkey’s large current-account swings and the idea that financing those gaps has at times relied heavily on drawing down official FX reserves.

Brooks links the vulnerability to political economy dynamics: in his view, sustained growth that heavily relies on imports — and policies that prioritise growth at almost any cost — can make the currency fragile, especially if authorities are willing to tolerate rising FX demand to preserve short-term growth and domestic political stability.

What Turkish strategists are saying: “Managed parity,” not a free float

On the domestic side, Dr. Atahan Çelebi — chief strategist at STRFS (Stratejistanbul Financial Solutions) — tells DW Türkçe that Turkey has not operated a fully free float since the 2001 crisis. Instead, recent years look more like a “managed” or “guided” exchange-rate regime: authorities, and ultimately the executive, still exert significant influence over the lira. That means the central bank’s interventions and the government’s posture can limit abrupt moves — at least until pressure becomes overwhelming.

Çelebi also emphasises that, when judged against long-term trends, the lira is not “extremely overvalued.” But he warns that trying simultaneously to fight high inflation and keep the currency steady is a policy contradiction that creates economic distortions — and can undermine external competitiveness.

Market expectations: one-year outlook edging higher

Data from the Central Bank of the Republic of Turkey’s Market Participants Survey shows a rising one-year FX expectation among professional respondents. In the September 2025 round, the 12-month dollar forecast moved up to about ₺48.96 from ₺48.36 in the prior round. Shorter-term end-year forecasts were broadly similar (around the mid-40s).

These figures reflect that corporates and financial market participants are pricing in some nominal depreciation over the coming year — but not an immediate, day-zero devaluation shock.

Political volatility and market responses

Political events continue to move markets. Borsa Istanbul’s sharp falls and rebounds over the past months — for example the 18% slide shortly after the detention of Ekrem İmamoğlu and the bounce after the postponement of the CHP congress hearing — underscore how politics and legal developments translate into risk premia and price swings.

Following the court postponement in mid-September, Turkey’s 5-year CDS spread fell to roughly 240 basis points — its lowest since February 2020 — showing short windows when risk perceptions ease. But experts caution that such improvements can be fragile.

Why most Turkish experts dismiss an imminent engineered devaluation

Marbaş Menkul Değerler’ chief economist Assoc. Prof. Dr. Caner Özdurak told DW Türkçe that he does not expect a sudden policy-led devaluation in the near term. His reasoning:

-

Policy mix: The central bank’s recent cuts — a 250-basis-point policy easing that put the policy rate at 40.5% — point to a deliberate disinflation and growth calculus. An abrupt, official devaluation would contradict the stated goals and would likely revive inflation and derail efforts to stabilise expectations.

-

Economic trade-offs: A deliberate, large devaluation would immediately raise inflation expectations and real-wage pressures, damaging domestic consumption and creating social as well as economic costs.

-

Political costs: For an administration already battling political and economic pressures, a policy that visibly erodes purchasing power through a sharp devaluation would be politically risky.

Özdurak does, however, stress that continued rate cuts will likely produce a gradual depreciation: “With further easing expected through the year, we will see some depreciation of the lira — but I don’t expect a deliberate policy to engineer a sudden, large devaluation. That would deliver more harm than benefit.”

What could force a sharper devaluation?

Although a deliberate, immediate devaluation is considered unlikely by many local economists, certain scenarios could make a sudden move more probable:

-

Reserves squeeze / funding shock: A major, sudden outflow of foreign capital or a big drop in FX inflows (for example from tourism or portfolio flows) could strain reserves and force sharper adjustment.

-

External shocks / trade disruptions: Rapid global rate moves, a significant slowdown in Europe (Turkey’s major trading partner), or a spike in commodity prices could widen the current-account gap and pressure the lira.

-

Political or credibility shock: A major loss of policy credibility — for instance if markets judge that fiscal and monetary policy are no longer aligned to stabilise inflation — could quickly amplify depreciation pressures.

-

Unanticipated policy U-turns: If authorities reverse course and opt for competitive devaluation as their principal tool to support domestic producers and exports, the market would rapidly price that in.

A middle path: gradual depreciation versus one-off devaluation

Most market analysts draw a distinction between a devaluation — an abrupt official re-setting of the currency peg or a decisive policy-driven revaluation of the exchange-rate regime — and depreciation, a market-driven or gradual decline in the currency’s value.

Current consensus skews toward the latter: a gradual, managed depreciation driven by continued rate cuts, inflation dynamics and episodic confidence shocks. An abrupt, policy-announced devaluation that instantly doubles or triples the exchange rate is viewed as a low-probability event in the immediate term — though not impossible if extreme shocks materialise.

Policy implications and what to watch

For investors, corporates and households, the near-term takeaway is to watch three key indicators:

-

FX reserves and reserve adequacy: Rapid falls in gross or net reserves would indicate loss of buffers.

-

Capital flows and FX funding lines: Any sudden stop or withdrawal of short-term funding would raise the urgency for adjustment.

-

Inflation expectations and real rates: As long as inflation expectations remain unanchored, the lira is vulnerable to episodic shifts.

If authorities can demonstrate credible, sustained disinflation while allowing a controlled easing of the currency, Turkey may avoid a disruptive devaluation. But if credibility erodes — or if external financing conditions worsen — the risk of a sharper, more disruptive adjustment will rise.

Bottom line: devaluation is not the base case — but vulnerability persists

In short, a sharp, deliberate devaluation is not the central scenario most Turkish economists and market participants currently expect. Experts such as Dr. Atahan Çelebi and Assoc. Prof. Caner Özdurak argue that political costs and economic side effects make a sudden devaluation an unattractive policy choice for Turkish authorities right now.

That said, Turkey remains exposed: its history of large current-account swings, political volatility, and the interaction between aggressive interest-rate cuts and high inflation mean that the lira is likely to face periods of volatility and gradual depreciation. The difference between a controlled adjustment and a crisis-driven devaluation will come down to reserves, market confidence and policy credibility in the months ahead.