Turkey’s Inflation Battle: Households Cut Food to Afford Rent as Rate Cut Hopes Fade

gelir dagilim

gelir dagilim

By Güldem Atabay

Adapted for English by PA Turkey Editorial Team

Rents Top Household Spending as Inflation Alters Living Standards

According to TurkStat’s 2024 Household Budget Survey, Turkish families are now spending more on housing and rent than any other category. Shelter costs accounted for 26% of household budgets nationwide, followed by transportation (23.6%) and food (18.1%). Notably, food—traditionally the largest spending category—has dropped to third place.

Among the poorest 20% of households, rent and food dominate expenses, comprising a staggering 72.1% of their total monthly consumption—38.4% goes to rent and 33.7% to food. In contrast, the wealthiest 20% allocate more to transportation and dominate spending in education, healthcare, and entertainment. High real interest rates are enabling this segment to preserve or grow wealth, thus sustaining domestic demand.

This widening consumption gap highlights a deepening inequality crisis in Turkey, especially under the pressure of persistent inflation. While high-income households benefit from tight monetary conditions, low-income groups are experiencing a cost-of-living emergency.

Wealth Gap Widens in Türkiye as Number of Millionaires Surges Past 2.3 Million

Income Inequality Now Unavoidable

The income divide is stark: the richest quintile now accounts for 47.7% of all consumer spending in Turkey, while the poorest 20% account for just 5.6%. The inequality is further underlined by inflation-adjusted spending figures: average monthly household expenditure rose to TRY 45,344 in 2024—up 86% from the previous year. Per capita spending rose 88.2% to TRY 23,558, far exceeding official CPI growth.

While wage-earning households spend 24% of their budget on rent, households dependent on entrepreneurial income allocate more to transportation. Compared to 2023, all key categories—rent, food, and transport—have seen significant cost increases.

As rent soars, food spending gets crowded out, limiting access to basic nutrition for low-income families. The inflationary burden is growing heavier for the majority, and consumption disparities are visibly escalating.

Inflation Eases, But Outlook Remains Murky

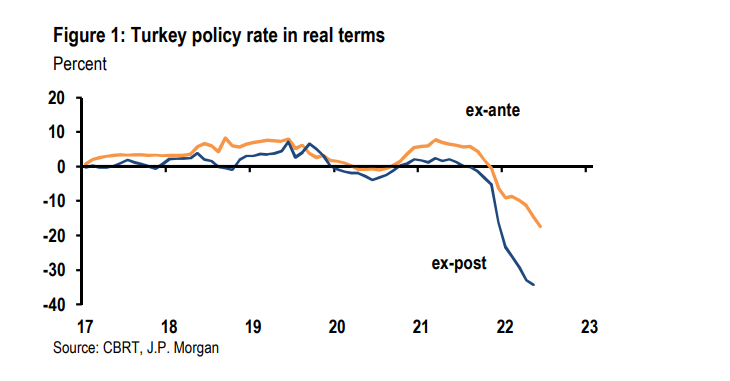

In May, Turkey’s CPI inflation surprised markets by slowing to 1.5% month-on-month, well below the 2.17% consensus estimate. However, producer price inflation (PPI) came in hot at 2.48%, driven by an 8% surge in energy prices.

While slowing domestic demand should reduce PPI-to-CPI passthrough, any premature rate cuts by the Central Bank of Turkey (CBRT) could heighten the risk of inflation persistence.

The details behind the CPI surprise point to anomalies. A 3% drop in unprocessed food prices—mainly fresh fruits and vegetables—helped pull headline inflation down. But this is likely temporary, influenced by unusual frost conditions in April. Meanwhile, core goods prices rose 3.3%, partially due to seasonal clothing hikes (+7.1%) and a 2.7% increase in durable goods (excluding gold).

The silver lining is that service inflation slowed to 1.7%. Rent inflation also eased to 3.1% in May—its lowest monthly increase in five months—though this remains aligned with trend inflation rather than the official target.

Don’t Be Fooled by May’s Soft CPI

Güldem Atabay: Time to Talk About an Industry-Focused, Tech-Driven Growth Initiative

The low CPI reading in May should not set expectations for continued disinflation. The CBRT’s own data supports this caution. Seasonally adjusted CPI rose 2.0%, and core inflation indicators (B and C) came in higher at 2.1% and 2.25%, respectively. Services inflation adjusted for seasonality was 2.6%, showing that underlying pressures remain strong.

The CBRT’s latest inflation assessment acknowledged a “gradual decline in core inflation trends,” based on three-month averages. But it avoided offering optimism beyond that. In fact, the central bank has become far more defensive in tone since the beginning of the political crackdown on CHP figures, which introduced fresh uncertainties into investor sentiment.

In short, May’s figures do not mark the beginning of a sustained disinflation trend. Summer and especially autumn will be the true test of inflation dynamics.

Growth Slows, But Not Enough for the CBRT’s Goals

Macroeconomic data already show that higher interest rates are slowing growth and hiring. But this slowdown may not be enough to bring year-end inflation in line with the CBRT’s official 24% target. Even the central bank itself has signaled acceptance of a higher ceiling, with its latest report implicitly revising expectations toward 29%.

Politics continues to cloud the picture. Ongoing tensions—especially the crackdown on opposition mayors and constitutional disputes—are increasing risk premia and maintaining pressure on the Turkish lira. Fiscal discipline also remains questionable, with high public spending and ballooning interest payments supporting consumption by wealthier households, further delaying disinflation.

If political volatility persists, the risk of economic “accidents” cannot be ruled out.

Rate Cut in June? Not So Fast

Talk of a June rate cut by the CBRT now seems disconnected from economic reality. After losing FX reserves during the March political turbulence (particularly following the arrest of Ekrem İmamoğlu), the CBRT hiked its policy rate to 50% and has been funding markets at an effective rate of 49%. That environment is hardly stable enough to permit easing.

Expectations are now shifting to July. But even then, the CBRT must proceed with caution. Before initiating cuts, it would first need to bring overnight funding rates back in line with the policy rate (currently 46%) and ensure no fresh demand for foreign currency is triggered.

For this to happen, Ankara must refrain from introducing new political shocks.

Defensive Posture, Not Policy Leadership

The CBRT has effectively moved from leading the fight against inflation to defending its last position. Political instability has forced the bank to prioritize stability over disinflation. With inflation expectations drifting higher and investor confidence rattled, real interest rates must stay elevated.

Assuming CPI ends the year between 33% and 35%, the policy rate can only be lowered modestly—from today’s 50% to perhaps 40% by year-end. A more aggressive cut to 38% would only be possible if CPI falls below 30%—a scenario not yet on the horizon.

Conclusion: The Cost of Survival

As Turkish families cut food expenses to pay soaring rents, the CBRT faces immense pressure from both political and economic fronts. Any hasty decision to ease policy could backfire, especially in an environment where inflation remains sticky, inequality is rising, and political risk remains high.

Disinflation is still possible—but only if Ankara stops adding to the fire.

IMPORTANT DISCLOSURE: PA Turkey intends to inform Turkey watchers with diverse views and opinions. Articles in our website may not necessarily represent the view of our editorial board or count as endorsement.

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/