ING: Turkey’s Policy Challenges Mount Amid FX Pressure and Reserve Concerns, Carry Still Attractive

tr-economy1

tr-economy1

Policymakers in Turkey are facing an increasingly complex economic environment as global uncertainty persists and local financial markets remain fragile. Despite some easing in commodity prices, recent FX volatility and a sharp depletion in central bank reserves have intensified pressure on authorities to act. ING’s latest report outlines both the hurdles and potential relief points as the country moves through the remainder of 2025.

Central Bank Tightens to Support Financial Stability

In the wake of March’s financial turbulence and reserve outflows, the Central Bank of Turkey (CBT) has taken several defensive steps:

-

A 200 basis-point hike in FX reserve requirement ratios, withdrawing over $7 billion from the banking system.

-

Exporters must now sell 35% of their FX revenues to the central bank (up from 25%) until July, which could support reserves by $2–2.5 billion monthly.

-

Banks are required to increase TRY deposit share among corporates, pushing for de-dollarization.

While the CBT’s key policy rate is 46%, effective funding is hovering near 49%, signaling a continued preference for tight monetary policy. Market watchers expect that any rate cuts will be conditional on renewed FX stability and a sustainable rebuilding of reserves.

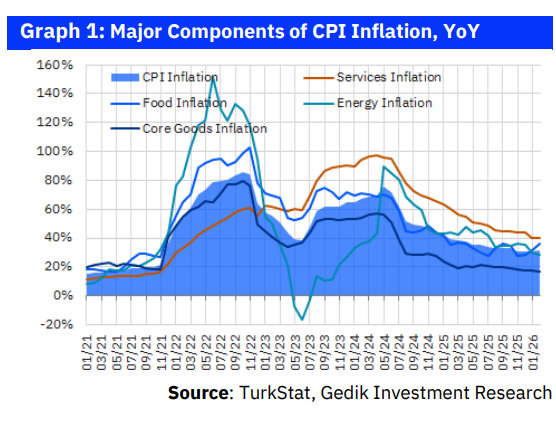

Inflation and the Road Ahead

April inflation surprised to the downside, giving a glimmer of hope, but the CBT’s inflation report on May 22 will be critical in clarifying future policy. ING still expects inflation to fall below 30% by year-end, assuming no new FX shocks, wage spikes, or energy price surges. Nonetheless, recent volatility has mildly damaged inflation expectations.

Meanwhile, the current account deficit widened again in February, driven by weaker trade. Preliminary data for March and April suggest further deterioration. External risks, such as US-China trade tensions and domestic political noise, continue to cloud the outlook.

FX View: TRY Stability Returns, For Now

The USD/TRY pair has resumed a controlled upward trend after the sharp spike in March. The CBT has reaffirmed its stance to prevent further FX-driven inflationary shocks and seems to have regained control of the currency trajectory.

The TRY continues to offer one of the most attractive carry trades in emerging markets, thanks to the central bank’s hawkish stance. While limited rate cuts may occur, ING believes they won’t undermine TRY’s appeal in the near term. The bank forecasts USD/TRY at 39.44 by mid-year and 43.00 by year-end.

Still, liquidity concerns persist in the forward FX market, which is why ING prefers the spot market for TRY exposure.

Government Bonds: Stabilization Will Take Time

After the March FX move, Turkish government bonds (TURKGBs) sold off sharply, particularly at the short end. The resulting curve flattening has persisted, with only marginal improvement.

Despite improved valuations — especially relative to Overnight Index Swap (OIS) rates — foreign outflows from Turkish bonds continued through mid-April. Investors seem to be waiting for stronger signals of sustained disinflation and more dovish messaging from the CBT before returning.

On the supply side, the Ministry of Finance has completed 37% of its planned 2025 issuance. However, with fiscal risks still lurking, most issuance remains concentrated in short maturities to avoid locking in high debt costs.

Sovereign Credit: Rating Optimism Paused, But Not Reversed

The recent policy response has helped reduce fears of a policy U-turn away from orthodoxy. Still, ING believes that credit improvements have now plateaued.

Markets will watch Moody’s July review closely, as the agency maintains a positive outlook but continues to rate Turkey one notch below its peers at B1. If market sentiment stabilizes, sovereign issuance on international markets could resume, offering further validation of Turkey’s re-engagement with global investors.

PA Turkey intends to inform Turkey watchers with diverse views and opinions. Articles on our website may not necessarily represent the view of our editorial board or count as endorsement.

Follow our English-language YouTube videos @REAL TURKEY: YouTube Channel

And content at Twitter: @AtillaEng