Gedik Macro View: CPI Inflation came in below expectations, strengthening the case for a July rate cut

inflation

inflation

July CPI inflation undershot expectations at 2.06% MoM, while annual CPI inflation eased to 33.5% from 35.0%. Headline CPI inflation in July was 2.06% MoM, somewhat below the 2.40% median expectation and our 2.25% estimate. With the relatively high July 2024 reading of 3.23% rolling out of the annual calculation, annual CPI dropped from 35.0% to 33.5%. This marked the continuation of the steady decline in annual inflation since its peak of 75.5% in May 2024. Core CPI inflation (Group C) came in at 1.74% MoM (vs. our 1.80% forecast and the 2.1% market median; July 2024: 2.45%), bringing the annual rate down to 34.7% from 35.6%. Domestic producer price inflation (D-PPI) maintained its moderate trend at 1.73% MoM (July 2024: 1.94%), pulling the annual rate slightly lower from 24.5% to 24.2%. As such, after two months of increases, annual D-PPI inflation edged down again in July.

The downside surprise appears to have stemmed from the clothing component. Looking into the sources of the below-consensus reading, the first thing that stands out is clothing inflation coming in at -6.0% MoM vs. our -%1.5% expectation. The divergence between the clothing item and other components has been widening with each release. Clothing prices are roughly 7% lower year-to-date and only 10% higher than a year ago. Since December 2021, cumulative headline CPI inflation stood at about 429%, while the clothing inflation has been just 130%. Over the same period, cumulative clothing inflation according to the Istanbul Chamber of Commerce (ICC) stands at 572%. This discrepancy is difficult to explain and may stem from methodological differences, potentially leading to a future revision in TurkStat’s methodology.

No major surprises outside the clothing component. Energy inflation came in slightly above our forecast (7.4% vs. 6.5%), while food inflation was marginally below our expectation (0.1% vs. 0.7%), broadly offsetting each other. Services inflation was in line with expectations at 3.1% MoM, close to our 3.0% forecast. Durable goods inflation and other core goods inflation were also in line with our projections. On a seasonally adjusted basis, we calculate that monthly CPI inflation was 2.5%, while services inflation reached 3.2%, both slightly higher than in previous months. On the other hand, core goods inflation continued to decline, supported by the clothing item. In short, the below-consensus headline figure reflects the idiosyncratic clothing impact rather than a change in underlying inflation dynamics. That said, we expect the market to focus more on the headline figure undershooting expectations, rather than the details, leading to continued positive pricing of today’s print in the coming days.

CBRT may continue with similar pace of rate cuts in September and October. As we have highlighted in our previous reports, while our year-end CPI forecast stands at 32%, we expect CPI to decline towards 30% (or slightly below) by September. In this context, the CBRT may proceed with further rate cuts of 250 – 300bps at its September 11 and October 23 MPC meetings, similar to the pace seen in July, taking the policy rate down to 37.0 – 37.5%. Thereafter, we expect the CBRT to adopt a more cautious stance monitoring FX demand dynamics and taking into account its end-2026 CPI forecast (midpoint 12%, in a 6 – 18% range)- and to proceed with smaller potential cuts in the subsequent period.

Related articles

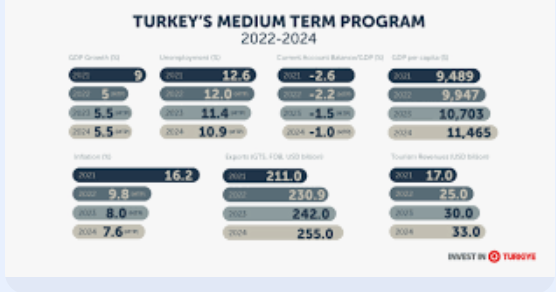

ANALYSIS: Turkey’s new Medium Term Economic Program, will it work?

Turkey September BoP: Solid surplus to continue, ample financing, but disturbing “unidentified” outflows

Analysis: January CPI surprised to the upside