SHOCKER: Fitch Downgrades Türkiye Outlook to Stable, Affirms Rating at ‘BB-’

fitch

fitch

Fitch Ratings has revised Türkiye’s outlook to “Stable” from “Positive” while affirming its long-term foreign-currency issuer default rating at ‘BB-’. The decision reflects a sharp decline in foreign exchange reserves following the Iran war and rising external vulnerabilities, even as the agency acknowledges the country’s strong economic fundamentals and resilient banking sector.

Outlook Downgraded on Reserve Losses

Fitch said the outlook revision was driven primarily by a significant drop in Türkiye’s international reserves since the start of the Iran conflict.

According to the agency:

- The Central Bank of the Republic of Türkiye (CBRT) has spent over $50 billion in FX interventions to support the lira

- A prolonged conflict could further strain external finances and fuel inflation

Türkiye’s large energy import bill remains a key vulnerability in this context.

Strengths and Constraints

Fitch highlighted several factors supporting Türkiye’s rating:

- A large and diversified economy

- Low government debt

- Continued access to external financing during periods of stress

- A resilient banking sector

However, these strengths are offset by:

- A history of high inflation

- Political interference in monetary policy

- Recurring balance-of-payments pressures

- Weak external liquidity

- Governance challenges

Atilla Yesilada: An Inconvenient Truth: No currency crisis, no devaluation in Turkey

Sharp Decline in Reserves

Türkiye’s external buffers have weakened notably.

- Gross international reserves fell to $162 billion in early April, from $210 billion at end-February

- Net FX reserves (excluding swaps) dropped to below $19 billion, from $79 billion

The decline was driven by:

- Non-resident capital outflows

- Increased FX demand from corporates

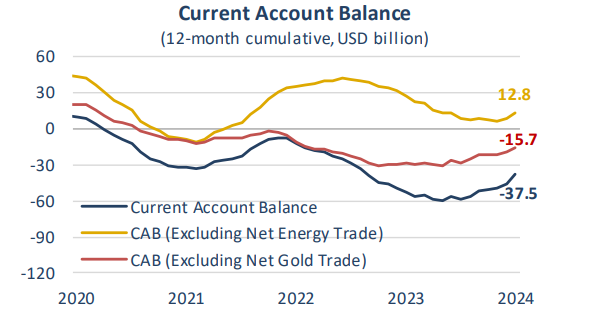

Current Account Deficit to Widen

Fitch expects Türkiye’s current account deficit (CAD) to increase in the coming years:

- 2.5% of GDP in 2026

- 2.9% in 2027

Higher energy prices and the lagged effects of real exchange rate appreciation are key drivers.

A further $20 increase in oil prices could widen the CAD by more than 1 percentage point of GDP, while also adding to inflationary pressures.

Dollarisation Remains Contained

The agency noted that deposit dollarisation has stabilized:

- Around 40% of total deposits

- Down from 73% in mid-2023 (including FX-protected deposits)

Authorities are expected to continue supporting lira demand through:

- Gradual depreciation

- Macroprudential measures

Tight Monetary Policy to Continue

Fitch expects monetary policy to remain relatively tight in the near term.

- Real policy rate projected at 5.5% by end-2026

- Easing to 2% by end-2027

However, risks remain that policy could loosen ahead of elections, potentially undermining stability.

Inflation Still Elevated

Inflation is forecast to remain high despite a gradual decline:

- 27% by end-2026

- 21% by end-2027

These levels remain among the highest for sovereigns rated by Fitch.

Elevated inflation expectations continue to pose risks, particularly if policy discipline weakens.

Geopolitical and Political Risks

Fitch said Türkiye has managed to balance its international relations during the conflict, with a low risk of direct military involvement.

However, risks remain from:

- Prolonged regional instability

- Domestic political developments

The agency noted that while market sensitivity to political shocks has declined, significant uncertainties persist ahead of the next elections.

High External Financing Needs

Türkiye’s external financing requirements remain substantial:

- $239 billion in external debt maturing over the next 12 months

External liquidity is expected to improve to around 98% by 2027, but this remains below the ‘BB’ peer median of 140%.

Growth and Fiscal Outlook

Fitch forecasts:

- GDP growth of 3.6% in 2026

- 4.2% in 2027

The general government deficit is projected to widen:

- To 3.7% of GDP in 2026

- To 4% in 2027

Public debt is expected to rise modestly but remain low relative to peers at around 26% of GDP.

Rating Sensitivities

Fitch said downside risks to the rating include:

- Further depletion of reserves

- Rising inflation and external imbalances

- Policy missteps or loss of confidence

Upside potential would depend on:

- Strengthening of external buffers

- Sustained disinflation and policy credibility

PA Turkey intends to inform Turkey watchers with diverse views and opinions. Articles in our website may not necessarily represent the view of our editorial board or count as endorsement.

Follow our English YouTube channel (REAL TURKEY):

https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/

Related articles

Turkey’s food prices skyrocket despite agriculture

Is Bank Research: Massive improvement in January current account deficit, more to come..

CBRT survey reveals Turkey’s year-end inflation is around 58 percent