Atilla Yesilada: Iran’s war, Türkiye’s headache

atilla9

atilla9

Tuesday morning, 02:00. Sleepless nights again. Fighter jets flying over Tehran enter my dreams. I am as sure as my own name that Trump and Netanyahu will attack Iran. As student protests erupt again in Iran and foreign currency shortages create new disruptions in trade, I find it naïve to assume these two war-obsessed leaders will leave their wounded prey alone. Iran constantly declares that it does not seek nuclear weapons, but is that officially the only demand of the U.S. and Israel? Therefore, nothing will come out of today’s talks either, and Trump could decide to strike at any moment.

I am soft-hearted; I would not want even an ant’s hair to be harmed. But an Iran war would mean a massive headache for Türkiye.

Let me first answer this question: despite perhaps the largest U.S. military buildup in the region since the Vietnam War, why is Iran refusing to negotiate? It has very valid reasons. Trump and Netanyahu are not reliable counterparts. If Iran were to end uranium enrichment and its ballistic missile program as Washington demands, and stop funding its regional proxies, it would become completely defenseless. It would be naïve to assume that Netanyahu — now transformed into a war demon — would not exploit such vulnerability.

Having concluded that negotiations cannot prevent an attack, Tehran has prepared plans to punish the U.S., Israel, and Arab states that fail to block them. The Strait of Hormuz would be closed to maritime traffic, reducing global energy trade by 20%. U.S. military installations in the region — especially in Qatar — would be targeted. If pushed further, Iran would strike energy production and transportation facilities along the Persian or Arab Gulf coast.

Naturally, its adversaries are aware of the risk of escalation and have developed their own strategies:

-

Assassinating Supreme Leader Khamenei to leave the regime leaderless. Potential successors might also be targeted.

-

Launching an intense bombing campaign to destroy all of Iran’s offensive military assets.

-

Disabling Iran’s navy on the first day to keep the Strait of Hormuz open.

-

Striking Revolutionary Guard and Basij headquarters, weapons depots, and even barracks to signal that civilians would not be harmed if they took to the streets.

-

Ultimately, imposing a naval embargo at the Indian Ocean exit of the Strait of Hormuz to block Iran’s energy exports to China — its sole source of foreign currency.

Five Kurdish Parties Form Political Alliance in Eastern Kurdistan

Would this be enough to collapse the regime? I think not. The regime holds military and economic power concentrated enough to control every nerve ending of society. My most likely scenario is that Iran turns into another Syria — peripheral provinces with Kurdish, Arab and other ethnic majorities breaking away from the center and launching armed rebellion. (I have not been able to assess the Azeri minority’s ties to the regime, but if they too seek separation, we could witness years of bloody conflict.)

The optimistic scenario would be the less-politicized Armed Forces taking control from the Revolutionary Guards and Basij. Perhaps Crown Prince Reza Pahlavi — whose popularity inside Iran I cannot measure — could assume temporary leadership.

Let me summarize. From the perspective of energy prices and the global economy, we face three scenarios:

-

Most likely scenario (50%): A prolonged U.S.-Israel bombing campaign, internal unrest, and Iran’s retaliation plans failing.

-

Second scenario (30%): Iran resists for several weeks and temporarily closes the Strait of Hormuz.

-

Worst-case scenario: Sabotage of Arab energy facilities and a U.S. naval embargo on Iranian oil exports.

In the latter two scenarios, sources I consulted estimate Brent crude could reach $100 per barrel. Even in the worst case, U.S. shale producers, Venezuela, and perhaps Russia could fill the supply gap — though this would take several months.

The global economy remains relatively strong. Composite PMI surveys from the Eurozone, Japan, and the U.S. suggest production remains resilient despite monthly fluctuations. Since energy’s share in global output has steadily declined since the 1974-77 oil crisis, I do not expect major growth losses outside a few countries.

However, inflation would rise. If China can no longer purchase discounted oil from Russia and Iran, inflationary pressures would be far more pronounced. In that scenario, emerging markets that do not issue reserve currencies or export commodities would likely pause rate cuts.

Bennett Calls Türkiye the “New Iran,” Urges Coordinated Strategy Against Ankara

Let us open a parenthesis. A regime collapse in Iran or Tehran turning fully inward to suppress uprisings would bring both advantages and disadvantages for Türkiye. The main advantages would include deeper integration of Iraq’s economy with Türkiye and the activation of the “Trump corridor,” boosting development in Azerbaijan and Türkiye. The disadvantage is a refugee wave. The Turkish Armed Forces have stated they are prepared to establish a security corridor on the Iranian side of the border if chaos erupts, but its effectiveness cannot be judged without actual migration flows. Wealthy Iranians buying property could also trigger domestic discontent.

Second, PJAK launching a “war of liberation” in Kurdish provinces has now materialized. On Monday, four Iranian Kurdish separatist organizations formally rebelled against the regime. The PKK could transfer its entire Kandil-based force into Iran. This would be positive for a terror-free Türkiye, but in the long term, the concentration of PKK elements along our border and the potential radicalization of our Kurdish citizens would deeply concern the security bureaucracy.

This is Türkiye’s headache

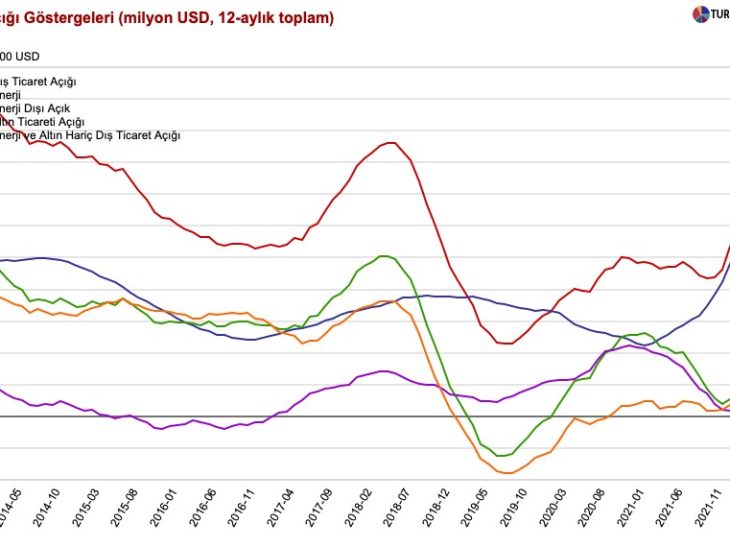

Leaving geopolitics aside, a rise in Brent to $100 per barrel could add up to 4 percentage points to inflation within a month. Higher energy prices would also pose risks to the current account. Yet even if war persists, I expect supply to outweigh demand and push Brent back into the $55-65 range within a few months.

A key point: for the current account to deteriorate seriously, energy prices must remain elevated throughout the year. But since pump prices are adjusted weekly, even a 3-4 week spike would lift next month’s CPI.

Moreover, according to CBRT research, headline inflation heavily influences inflation expectations. In other words, even a short-lived oil surge can entrench inflation. Worse still, opportunistic producers and retailers may impose excessive price hikes during the oil rally and fail to reverse them when oil retreats.

We live in an interconnected world. Bombs falling on Iran would wound Türkiye’s stabilization program as well.