Market Outlook: Global Markets Brace for Nvidia Earnings as Tech Sell-Off Deepens

nividia

nividia

Global markets entered Wednesday on edge as a broad technology sell-off, rising bond yields, and renewed policy uncertainty pressured risk appetite. Investors worldwide are now focused on Nvidia’s earnings report, widely seen as the next major catalyst for equity sentiment. Meanwhile, expectations of fresh fiscal stimulus in the United States and Japan have driven bond yields higher, boosted precious metals, and amplified volatility in cryptocurrencies. Turkish markets remained relatively steady, though concerns persist over parts of the domestic fund industry.

Tech Stocks Under Pressure as Valuation Concerns Mount

The week opened with heavy selling across Asian markets, led by technology shares. That pressure eased slightly on Wednesday, but sentiment remains fragile ahead of Nvidia’s closely watched earnings release.

The Nasdaq Composite has fallen roughly 2% over the past two sessions, with futures remaining in the red on Wednesday. In Asia, the Tokyo Stock Exchange’s benchmark index slumped 3.2% on Tuesday before stabilizing in flat trade.

Investors fear that elevated valuations across the artificial-intelligence complex could leave markets exposed if Nvidia delivers anything short of a blowout performance. The chipmaker, considered the “heavyweight” of the AI boom, is expected to influence risk appetite beyond the tech sector and across global markets.

US and Japan Fiscal Expectations Drive Bond Yields Higher

Bond yields in the United States and Japan climbed as markets reassessed the likelihood of near-term rate cuts and priced in the potential for new government spending.

In the U.S., expectations for a Federal Reserve rate cut in December have weakened significantly. Meanwhile, President Donald Trump’s declining approval ratings have revived speculation that he could pursue additional fiscal measures to support households.

Trump has floated the idea of distributing tariff revenues to citizens as a “tariff-based dividend,” suggesting payments of at least $2,000 per person, excluding high-income households.

Japan is facing a similar narrative. Proposed stimulus measures by Prime Minister Sanae Takaichi’s government—including a supplementary budget exceeding 25 trillion yen—are placing upward pressure on long-term Japanese government bonds. The 10-year JGB yield has climbed to a 17-year high, and markets are watching Wednesday’s 20-year bond auction for further signals.

The divergence in global bond markets pushed the Japanese yen to its weakest level of the year against the U.S. dollar.

Precious Metals Surge as Inflation and Liquidity Risks Rise

Expectations of expanded fiscal spending in the U.S. and Japan have lifted inflation concerns, leading to fresh selling in long-term bonds—and renewed demand for hard assets.

Gold has approached $4,100 per ounce, reclaiming ground near its historic highs. Silver has once again tested $51 per ounce, supported by both safe-haven flows and industrial demand expectations.

Analysts argue that the fundamental case that drove gold from $2,000 to above $4,000 remains fully intact, citing ongoing geopolitical uncertainty, fiscal loosening, and long-term erosion of real yields.

Silver, long considered undervalued relative to gold, is gaining attention for its catch-up potential. A decisive break in the gold-to-silver ratio below 77.50—currently near 79—could trigger a sharp move in favor of silver, analysts say.

Crypto Weakness Persists as Bitcoin Breaks Key Support

Cryptocurrencies remain under pressure. Bitcoin failed to hold the $108,000–$109,000 support band, and after losing the $96,000–$97,000 region as well, briefly dipped below $90,000 before stabilizing near $91,000 on Wednesday morning.

Risk aversion, declining liquidity, and long-term bond volatility have all contributed to the weakness. Yet analysts caution against a myopic view: U.S. discussions about broader sanctions on China, Russia, and Iran—as well as debate about alternatives to SWIFT—remain supportive for blockchain-based financial infrastructure in the medium term.

Gold/Bitcoin spreads have widened consistently in gold’s favor for four consecutive months.

Trump–Powell Tension Escalates as Fed Leadership Question Looms

The escalating tensions between President Trump and Federal Reserve Chair Jerome Powell have added further uncertainty to the policy outlook.

Trump has intensified his criticism of Powell, stating:

“I would like to fire him, but they won’t let me.”

Powell’s term expires in May, and markets expect heightened political pressure as the deadline approaches. Treasury Secretary Scott Bessent said Trump will meet potential candidates for Fed Chair after Thanksgiving, with a final decision expected before Christmas.

Analysts warn that if a future Fed Chair were to pursue aggressive rate cuts—similar to Turkey’s 2021 experience—the likely consequences would include higher inflation, wider fiscal deficits, and renewed dollar weakness.

Model Portfolio Strategy: TL-Dominant, Metals-Heavy Allocation

Given the current macro backdrop, analysts highlight the following model portfolio allocation as prudent:

-

40% Turkish lira (time deposits or high-quality money market funds)

-

20% gold

-

20% silver

-

10% U.S. equities

-

10% Bitcoin (via Nasdaq-listed IBIT)

The strategy prioritizes inflation protection, liquidity, and diversification across uncorrelated assets.

Turkish Markets Steady but Fund-Sector Questions Persist

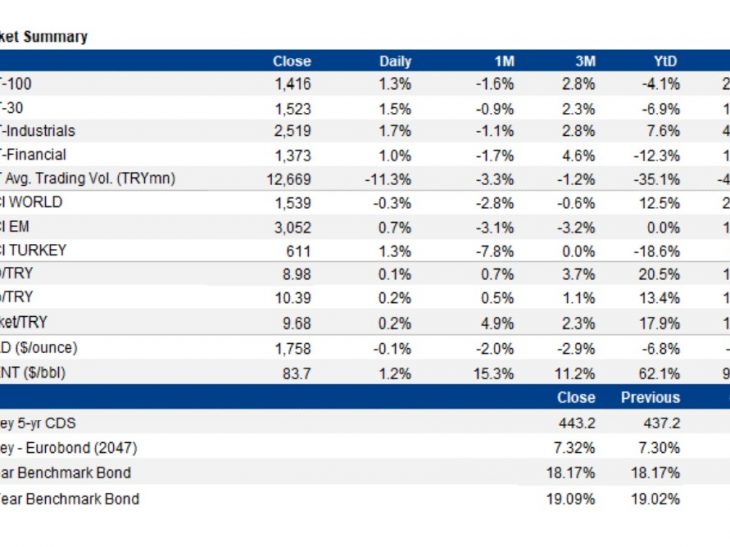

Borsa Istanbul’s BIST 100 index ended Tuesday slightly higher, while trading volumes remained moderate. The USD/TRY rate continued its slow upward drift toward 42.33, supported by strong central bank reserves.

Turkey’s five-year CDS risk premium remains pinned between 245–250 basis points, a tight range suggesting limited near-term volatility.

However, lingering concerns around certain domestic investment funds continue to generate debate. Analysts expect at least a verbal intervention from regulators to reassure markets. Most observers emphasize that the broader fund industry remains solid and does not face systemic risks, though poorly managed products could be phased out.

Markets Look to Fed Minutes and US Jobs Data

The S&P 500 has fallen for four consecutive sessions as U.S. data points to potential softening in the labor market. Initial jobless claims rose sharply from mid-September to mid-October, raising investor caution.

Following the government shutdown on October 1, the first batch of economic data has been weaker than expected. Investors will be watching:

-

Tonight’s release of the Federal Reserve meeting minutes, and

-

Thursday’s delayed non-farm payrolls report,

for clues about the December policy meeting.

Futures markets currently assign a 47% probability to a 25-basis-point rate cut in December, though divisions within the Fed cloud the outlook.

Analysts interpret much of the latest selling as year-end position trimming, not a decisive trend reversal.

By Emre Degirmencioglu, Cyprus Iktisat Bank

PA Turkey intends to inform Turkey watchers with diverse views and opinions. Articles in our website may not necessarily represent the view of our editorial board or count as endorsement.

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/***