Gedik Investment Weekly Monetary Aggregates Report

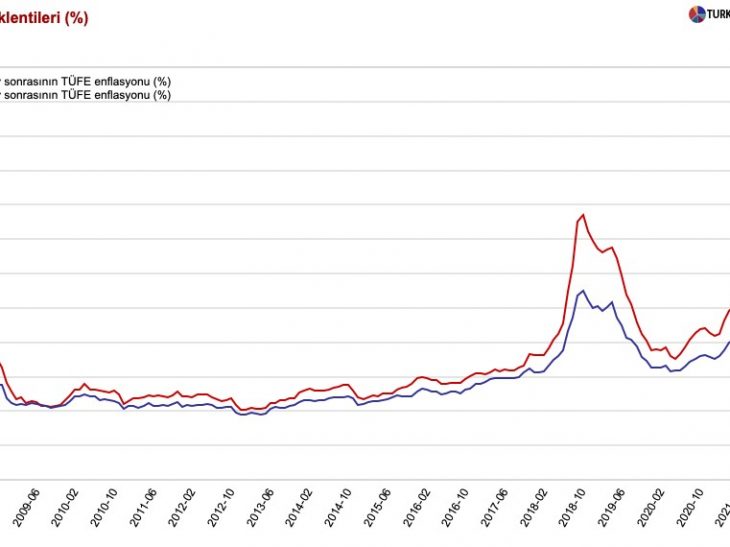

cbrt-resrves-17sept

cbrt-resrves-17sept

In the week of week of September 12, a USD 2.5 billion decline in net reserves excluding swaps (USD 4.9 billion decline adjusted for gold prices), a USD 588 million purchase of government domestic debt securities (GDDS) by non-residents, and a USD 1.4 billion increase in FX deposits stood out. Additionally, according to the CBRT’s Analytical Balance Sheet, as of September 17 (covering the first three business days of the week), we estimate an increase of approximately USD 0.6 billion in net reserves excluding swaps.

The weekly developments can be summarized as follows:

➢ Parity-adjusted FX deposits rose by a total of USD 1.4 billion, with USD 795 million in individual purchases and USD 644 million in corporate purchases. Since the beginning of the year, FX deposits have increased by a total of USD 16.3 billion.

➢ FX-protected deposit (KKM) balances decreased by TRY 23.2 billion (USD 0.6 billion) on a weekly basis, falling to TRY 345 billion. The cumulative unwinding from the peak reached in August 2023 has now exceeded TRY 3 trillion (USD 128.4 billion). The share of FX deposits + KKM in total deposits fell from 40.2 % to 39.9 %. At its peak in August 2023, this ratio had reached as high as 68.4 %.

➢ TRY deposits increased by TRY 343 billion over the week, rising to approximately TRY 15.1 trillion.

➢ FX loans rose by USD 0.2 billion on a weekly basis. Since the end of March 2024, they have increased by 44 % (USD 59.4 billion) to reach USD 194.1 billion.

➢ Looking at the annualized 13-week average loan growth, commercial loans slowed from 22.3 % to 21.2 %, while consumer loans declined from 43.5 % to 41.6 %.

➢ In the week ending September 12, non-residents recorded a net purchase of approximately USD 588 million in GDDS, bringing the stock to around USD 15 billion. Between mid-March and the end of April, GDDS saw a total outflow of USD 9.3 billion, while from the beginning of May onward, there has been an inflow of approximately USD 4.9 billion.

In equities, there was a net sale of USD 165 million, reducing the stock to USD 31 billion. Since the week of April 18 (excluding the week of June 20), equities had seen consistent weekly inflows, but this reversed over the past three weeks. On the Eurobond front, there was a net sale of about USD 18 million, bringing the stock to approximately USD 78.4 billion.

➢ Gross international reserves declined from USD 180.1 billion to around USD 177.9 billion, a weekly decrease of roughly USD 2.2 billion. In the same week, net reserves fell from USD 71.2 billion to about USD 69.6 billion, a decrease of USD 1.6 billion. Net reserves excluding swaps decreased by USD 2.5 billion to around USD 51.8 billion. It is worth noting that the increase in gold prices generated a positive valuation effect of USD 2.4 billion on the CBRT’s reserves last week. Accordingly, excluding this gold-price impact, the decline in net reserves ex-swaps would amount to USD 4.9 billion. For reference, the lowest point of net reserves ex-swaps was USD -65.5 billion at end-March 2024, while the peak was USD 71 billion on February 14, 2025.

➢ Based on the CBRT’s Analytical Balance Sheet, as of September 17 (the first three days of this week), we estimate that gross reserves and net reserves each increased by about USD 0.5 billion, and net reserves ex-swaps rose by roughly USD 0.6 billion. During this period, the gold-price effect amounted to around USD 0.4 billion. The cumulative positive contribution of higher gold prices to CBRT reserves over the past four weeks has now reached approximately USD 8.5 billion.

➢ The size of the Money Market Fund (MMF) increased by about TRY 55 billion during the week of September 12, rising to approximately TRY 1.2 trillion. Under the Free Umbrella Fund, MMFs decreased by roughly TRY 42 billion over the past week, falling to TRY 1.1 trillion. The total active size of FX-denominated mutual funds increased by USD 1.5 billion during the week, reaching approximately USD 68 billion. This figure was around USD 25 billion at the beginning of 2024. Including investment funds, the dollarization ratio declined from 42.5 % to 42.4 % in the week of September 12. This ratio had stood at approximately 59 % at the beginning of 2024.

Related articles

Turkey’s inflation falls to 55.2 percent in February

Dorian Jones: Erdogan hopes a U-turn can salvage Turkey’s floundering economy

Turkey to Launch ‘Citizenship Wage’ in 2026: A Structural Reform in Social Welfare